Brief thoughts on APP: AppLovin Corporation

How they make money, Bull and Bear Case, Q4 highlights and Am I opening a position?

AppLovin Corporation engages in building a software-based platform for mobile app developers to enhance the marketing (user acquisition) and monetisation of their apps in the United States and internationally.

They have been enjoying massive growth following the successful launch of its AXON 2.0 AI engine, which has significantly improved the efficiency of mobile advertising. N.B. they have divested their first-party gaming studios to focus entirely on its higher-margin Software Platform.

How they make money:

Performance Advertising: The majority of revenue comes from advertisers paying on a Cost-Per-Install (CPI) basis. Because AXON 2.0 is so effective at matching ads to users, AppLovin can charge a premium while still delivering a high Return on Ad Spend (ROAS) for the client.

Platform Fees: They collect a percentage of every ad transaction that passes through the MAX auction system (mediation fees).

SaaS Subscriptions: They generate recurring revenue through the Adjust analytics platform.

Bull case:

AI Dominance (AXON 2.0): The AXON engine has created a “moat” by delivering significantly better conversion rates than competitors like Unity. This has led to Adjusted EBITDA margins exceeding 80% in the software segment.

E-commerce Expansion: Their partnership with Shopify allows them to help physical product brands target mobile gamers, opening a massive new Total Addressable Market (TAM).

Strong Cash Flow & Buybacks: They generate billions in free cash flow (FCF), which they have used to aggressively repurchase shares (over $2.5B in 2025 alone).

Financial Momentum: Their Q4 2025 report (released Feb 11, 2026) showed 66% YoY revenue growth, crushing Wall Street estimates and providing bullish guidance for 2026.

Bear Case:

Short-Seller Allegations: Multiple short reports that have alleged its growth is inflated by fraudulent traffic or “money laundering” schemes. While management denies this and no proof has surfaced, the overhang of these reports causes volatility. Note a recent short report was withdrawn after the stock fell, and they apologised. Likely they flipped long.

Platform Risk: They are ultimately at the mercy of Apple (iOS) and Google (Android). Any significant change to privacy rules or how ads are served on these operating systems could cripple AppLovin’s tracking capabilities.

Competition: Tech giants like Meta and Google are ramping up their own AI tools (Project Genie) to reclaim market share in the mobile gaming space.

Q4 and FY 25, Key Financial Highlights

Q4 2025 Revenue: $1.66 billion, up 66% year-over-year.

Q4 2025 Adjusted EBITDA: $1.4 billion, up 82% year-over-year, with an 84% margin.

Full Year 2025 Revenue: $5.48 billion, up 70% year-over-year.

Full Year 2025 Adjusted EBITDA: $4.51 billion, up 87% year-over-year, with an 82% margin.

Q4 2025 Free Cash Flow: $1.31 billion, up 88% year-over-year.

Full Year 2025 Free Cash Flow: $3.95 billion, up 91% year-over-year.

Share Repurchases (Full Year 2025): Approximately 6.4 million shares for $2.58 billion, funded by free cash flow (effectively returned nearly 65% of its annual Free Cash Flow to shareholders via buybacks in 2025)

Rule of Forty Score: 150 (66% revenue growth + 84% Adjusted EBITDA margin).

Some charts:

Guidance

For the first quarter of 2026, AppLovin expects revenue to be between $1.745 billion and $1.775 billion, representing a sequential growth of 5%-7%. Adjusted EBITDA is projected to be between $1.465 billion and $1.495 billion, maintaining an Adjusted EBITDA margin of approximately 84%. Extreme Operational Efficiency.

This outlook reflects continued strength in gaming, the scaling of e-commerce, and the impact of new features like the prospecting model, partially offset by typical Q1 seasonality.

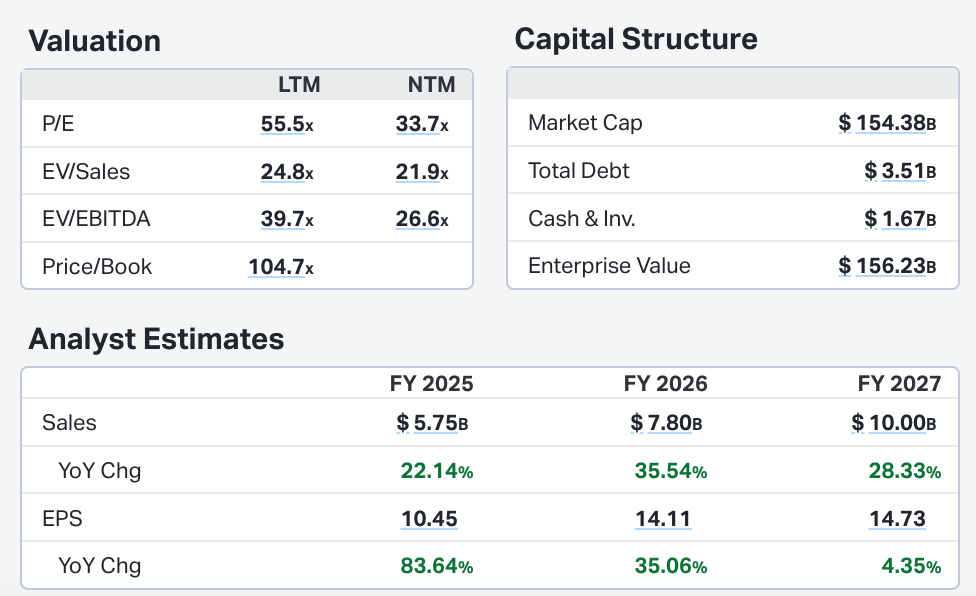

Valuation:

At current levels, $APP is trading at 25x EV/EBITDA despite growing EBITDA at over 80%. While the sales multiple appears optically rich at ~20x, it is justified by the stelar growth, an Adjusted EBITDA margin exceeding 80% and a robust 75% operating margin

Final Thoughts and my plans: