INTC Up 100%: Revisiting the Jan 27 Trade Idea

Responding to subscriber messages

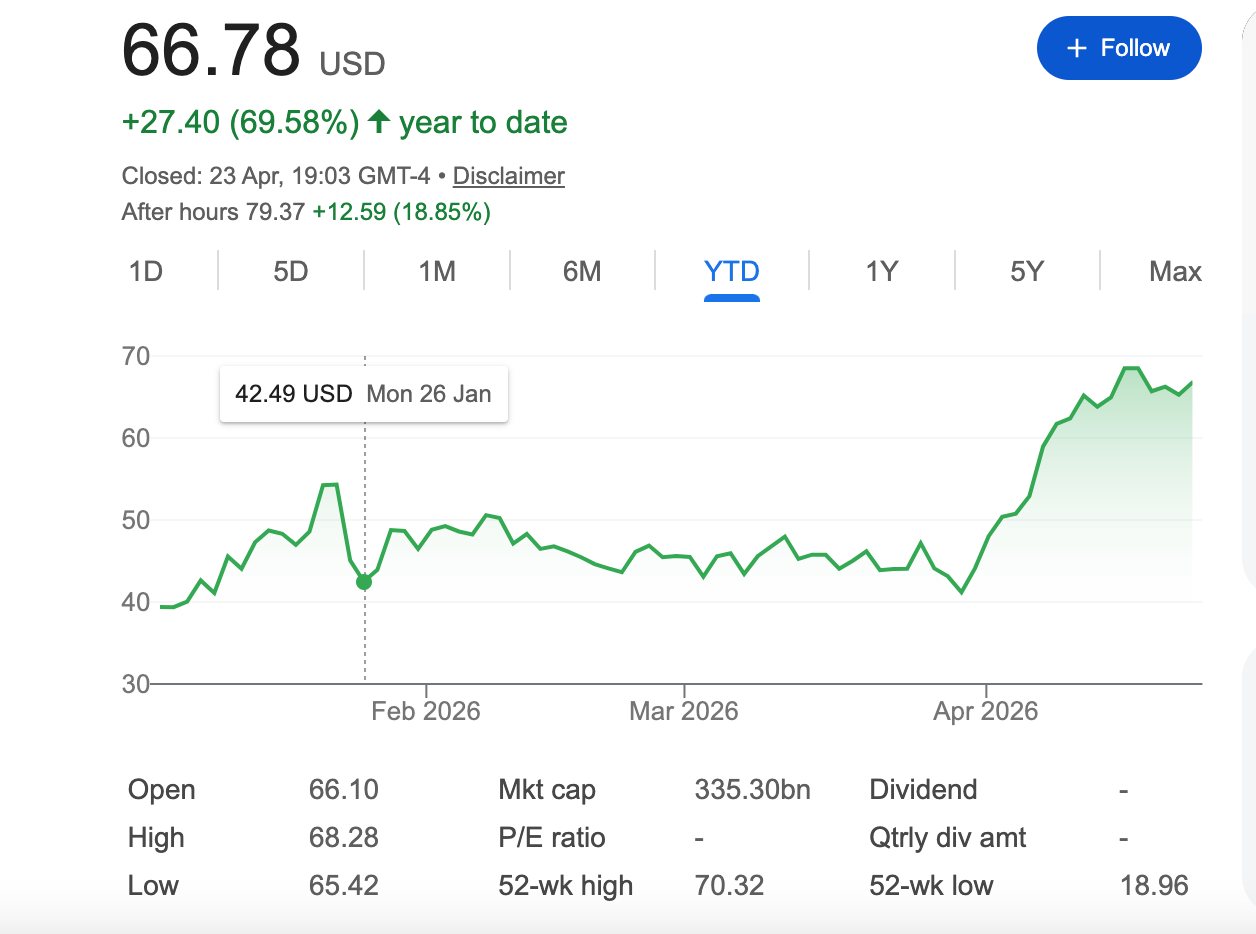

I’ve received a few messages from readers regarding my January 27th Intel long pitch, specifically asking what I’m currently doing and what they should do. I’ve included the original post below for those who may have missed it (link and also transcript further below)

Firstly, congrats to those who took the trade; being up 100% is no small feat! The earnings were fantastic and so was the guide.

Regarding my own position, I bought the day after the pitch at $41 as per my logs; however, I ended up selling at around $50/share in early February. So, while I did capture some of the move, I definitely left a lot of money on the table. In the CPU space, I am still in ARM which I shared recently at $159, now around 220.

How to manage the position? Not financial advice, but generally, if you feel a position is extended, trimming and trailing is the way to go.

INTC Trade Idea Jan 27:

”Below are some thoughts on a potentially interesting trade set-up that is forming.

Intel (INTC) shares have plummeted nearly $20 following its Q4 earnings report. While the company delivered a beat on both revenue and EPS, the results were overshadowed by a cautious Q1 outlook. This guidance highlighted persistent supply constraints and margin pressures linked to Intel’s ongoing manufacturing transition.

Financials

Q4 Revenue: $13.7B (Beat)

Q4 Non-GAAP EPS: $0.15 (Beat)

Q1 Revenue Guidance: $11.7B – $12.7B

Non-GAAP Gross Margin: Slipped to 37.9%

Management expects available supply to trough during the current quarter, which is weighing on short-term sentiment.

Bull Case & Setup

IMO, the long-term bull thesis for Intel rests on three strategic pillars:

The 18A Roadmap: Reclaiming transistor leadership through the 1.8nm node, representing Intel’s first real chance to leapfrog competitors in process technology in a decade.

The De Facto “Western Foundry”: Positioning as the premier U.S.-based manufacturing alternative, reinforced by the historic 9.9% equity stake held by the U.S. Government.

Cyclical Tailwinds: Capitalising on the dual demand of the Server CPU refresh and the massive AI PC hardware cycle.

Despite the immediate post-earnings volatility, the “on-shoring” narrative remains a structural trend. As global demand for high-end domestic foundry capacity grows, Intel’s role as a national champion provides a unique valuation floor that few other semiconductor plays can claim.

A fundamental snapshot does not reveal INTC to be especially cheap (see below), but the bottom line is expected to grow significantly and a surprise Apple announcement could cause a material upward revision of estimates.

Technicals

From a trading perspective, tomorrow marks Day 3 post-earnings, often a turning point for institutional ‘washout’ selling (the 3-day rule). Notably the ATR has been much higher than usual at 6.86% for the last 14 days versus the 100 day average of 3.91%.

The stock is currently approaching its 50-day SMA ($40.13). It is within one ATR of the SMA 50. This level represents a potential area of interest to initiate a long, using a definitive break below the 50-day SMA as a logical stop-loss to manage risk.

I have no position yet, but I am very tempted to initiate one in my trading account should it come in a little more towards the $40 zone. Conversely, I may wait to see if it can consolidate for a short period, but given the whipsaw market we find ourselves in, it often pays to act quickly.

As always, not financial advice just a potential set-up I am watching!”

Thank you for reading and see you for the next one!

It’s not going to back to 40s mate