Monthly Portfolio Update: +447.40% TWR Since 2023 (+345.6% Outperformance vs. S&P 500)

Market Thoughts | +345.6% Performance Since Inception | 2026 Position Plans & Outlook.

I hope you are well. Below, we provide market commentary and an in-depth portfolio update.

Format for what is covered in this Monthly Portfolio Update:

Market Thoughts

Indices Review

Key Indicators

SixSigmaCapital Performance: YTD and since Inception

Featured Quote

Current Positions in size order

Closing Thoughts

If it is your first time here, ensure to check out what SixSigmaCapital readers are saying below:

For all readers a reminder that a premium subscription includes:

Live Portfolio updates (All Buys and Sells) in Subscriber only Channels

Favourite set-up Ideas, Market Memos plus Full archive

Discord access for AMAs and live trading account updates (Annual Subscribers only)

Monthly in depth portfolio & performance updates

Upgrade to a premium subscription via the link below:

Market thoughts:

Equity markets had another strong month in May, with the Dow, S&P 500, and Nasdaq Composite posting month-over-month returns of +3.1%, +5.3%, and +8.9%, respectively.

For the last several months, I have been saying the following in this letter:

My perspective remains that there is plenty to be concerned about regarding the US economy and equity markets over the medium term” and

“Historically, there tends to be a large drawdown in the S&P 500 within the 12 months preceding election day. I do not know whether it will be Fed-related, a policy shock by the White House, or an economic downturn that triggers the drawdown (or something else entirely), but I think it is very likely we will see one given the way markets are behaving”

In the last year markets continued to climb the wall of worry though the indices finally cracked in March. The S&P 500 pulled back more than 9% peak-to-trough, and the Nasdaq fell 13%. Although this may seem modest compared to other pullbacks, significant damage was done under the hood: at the end of March, more than 42% of S&P 500 stocks were in a bear market, with more than 79% trading below their 50-day SMA. Consumer Discretionary, Information Technology, and Financials were among the worst performers in Q1, while Energy was the best performer.

However, April and May brought a historic rebound. From the March 30 lows until the end of May, the S&P 500 gained more than 1,300 points (greater than 15%), while the Nasdaq Composite surged 6,300 points from its bottom (an advance of more than 30%). Both indexes ended the month of May at all-time highs. June has got off to an interesting start, more on that next time.

Beyond this, semiconductors and every layer of the tech supply chain are on a historic run; the SOXX ETF ended May up more than 85% since its March lows, leaving semiconductors as a group at their most overbought levels in history. In fact, they are even more overbought than they were during the dot-com bubble or the COVID-19 mania!

Before we forget, we are still seeing a stagflationary picture with up-ticking inflation, tapering GDP, and a generally weakening jobs market (the most recent NFP report notwithstanding). Notably, large companies are conducting layoffs en masse.

Unpopular view but I feel the aftermath war in the Middle East will likely serve as further headwinds in the coming months. If we look at oil specifically, I backtested what happens to equity markets when crude remains consistently above $100; I found that stocks can remain robust for around 20 days, but after that, they tend to suffer. This is something to pay attention to as we head into the rest of summer, though crude is currently at $90 after pulling back.

While we saw a correction in March, it remains to be seen if that was the major midterm election-year pullback or if another one will occur later in the year. Notably, S&P 500 earnings estimates continue to be revised upward, and the majority of companies are beating expectations and raising guidance. This fundamental strength argues against a large, index-level pullback; however, a retrace to the 50-day simple moving average or even the 7,000 breakout level on the SPX is not out of the equation. If a meaningful pullback does materialise, I will certainly be a buyer of select equities.

Inflation:

CPI: The April 2026 CPI data is presented below

Headline CPI increased 3.8% YOY vs expectations of 3.7% YOY.

Headline CPI increased 0.6% MOM vs expectation of 0.6% MOM.

Core CPI increased 2.8% YOY vs expectations of 2.7% YOY

Core CPI increased 0.4% MOM vs expectations of 0.3% MOM

PPI: The April 2026 PPI data is presented below

Headline PPI increased 6.0% YOY vs expectations of 4.9% YOY.

Headline PPI increased 1.4% MOM vs expectation of 0.5% MOM.

Core PPI increased 5.2% YOY vs expectations of 4.4% YOY

Core PPI increased 1.0% MOM vs expectations of 0.4% MOM

The headline figure was driven by a sharp rise in energy prices.

Below I have included charts showing the trend for both CPI and PPI:

PCE: With regards to the PCE price (Fed’s preferred metric), March ‘26 data came in largely as expected but showed re-acceleration, with core at its highest since late 2023.

Headline PCE increased 3.8% YOY vs expectations of 3.8% YOY.

Headline PCE increased 0.4% MOM vs expectation of 0.5% MOM.

Core PCE increased 3.3% YOY vs expectations of 3.2% YOY

Core PCE increased 0.2% MOM vs expectations of 0.2% MOM

Whilst Core PCE came in lighter than expectations, Core PCE has proven notably sticky throughout the last year.

FOMC Meeting:

At the most recent FOMC meeting on April 28-29, 2026, the FOMC decided to hold interest rates steady for a third consecutive meeting as they navigate persistent inflation and a cooling labor market. The target range for the federal funds rate remains at 3.5% to 3.75%.

Interestingly, there were four dissents , the most since 1992. One for a 25bp cut and three against the “easing bias” language used.

The Committee reiterated that it is attentive to risks on both sides of its dual mandate (price stability and full employment). While energy costs are keeping inflationary pressure up, there are concerns that higher fuel prices will dampen disposable income and slow overall GDP growth.

No SEP projections were released, as they are only published quarterly.

Indices:

S&P 500

Currently trades at 7,383.74 (7.66% YTD)

It is 3.18% above the 50SMA.

Trading at 25.73x trailing earnings and 22.19x forward earnings (per WSJ)

Nasdaq Composite:

Currently trades at 25,709.43 (10.65% YTD)

It is 3.78% above the 50SMA.

Trading at 35.28x trailing earnings and 27.27x forward earnings (per WSJ)

Key Indicators:

10 Year T-Note: 4.536. It has increased by 8.34% YTD

British Pound vs USD: 1.334 and is down 0.83% YTD.

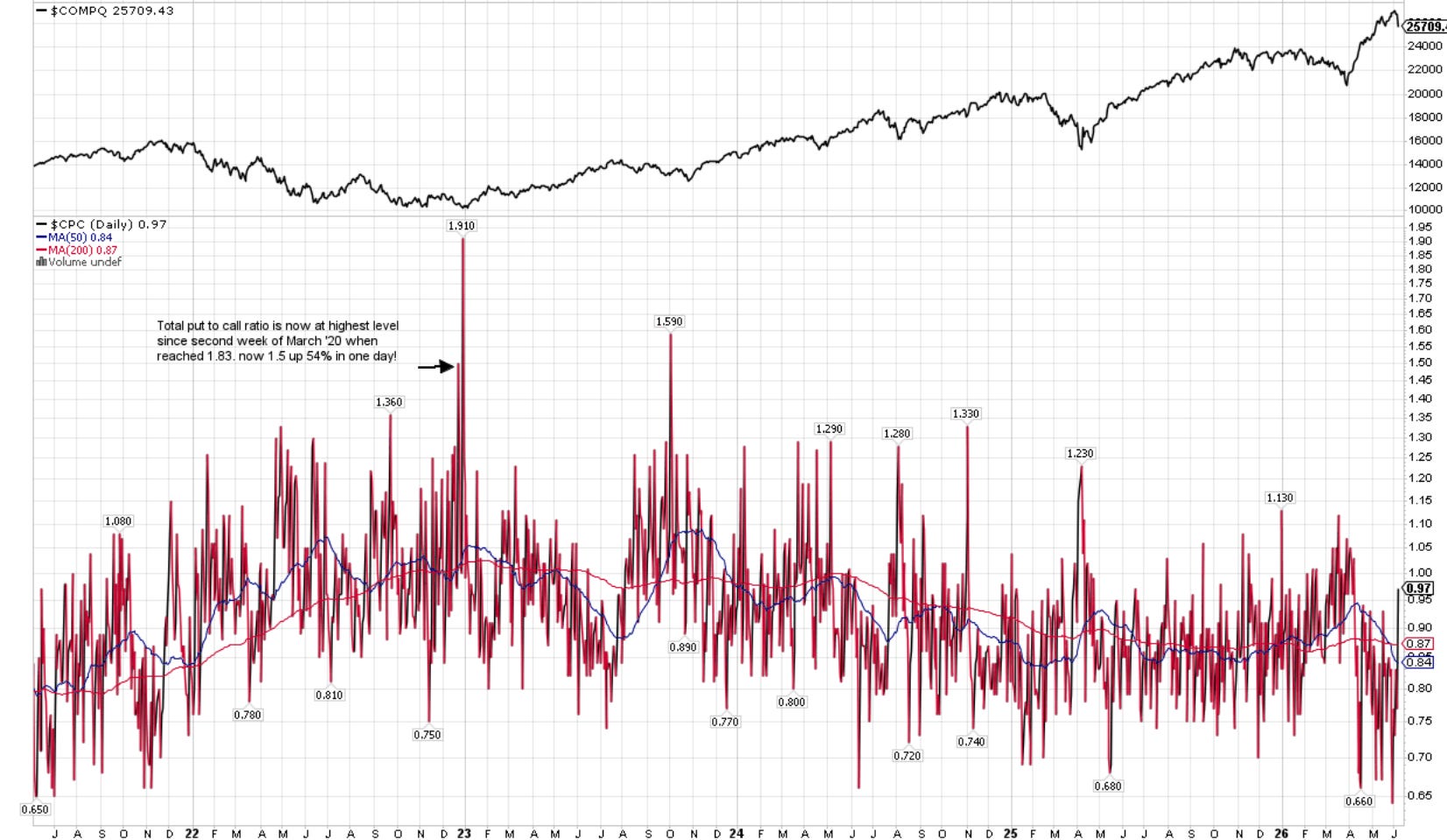

CPC (Put to Call Ratio) is 0.97. Note >1 can indicate Fear and >1.5 can be Extreme.

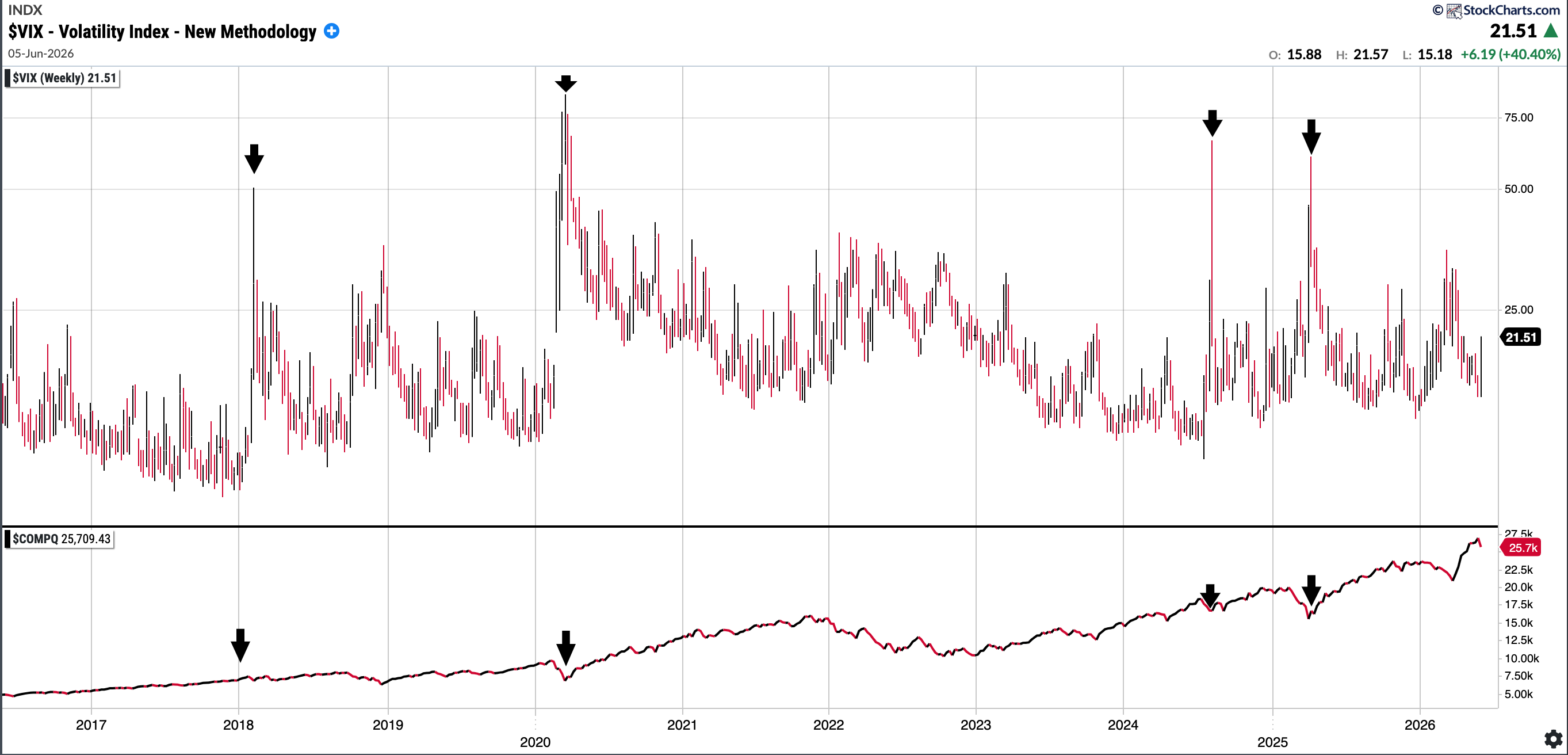

VIX: 21.51. I have included a chart below showing the VIX over time and Nasdaq Comp underneath it: you can see that extreme readings have always been a buying opportunity in the medium term.

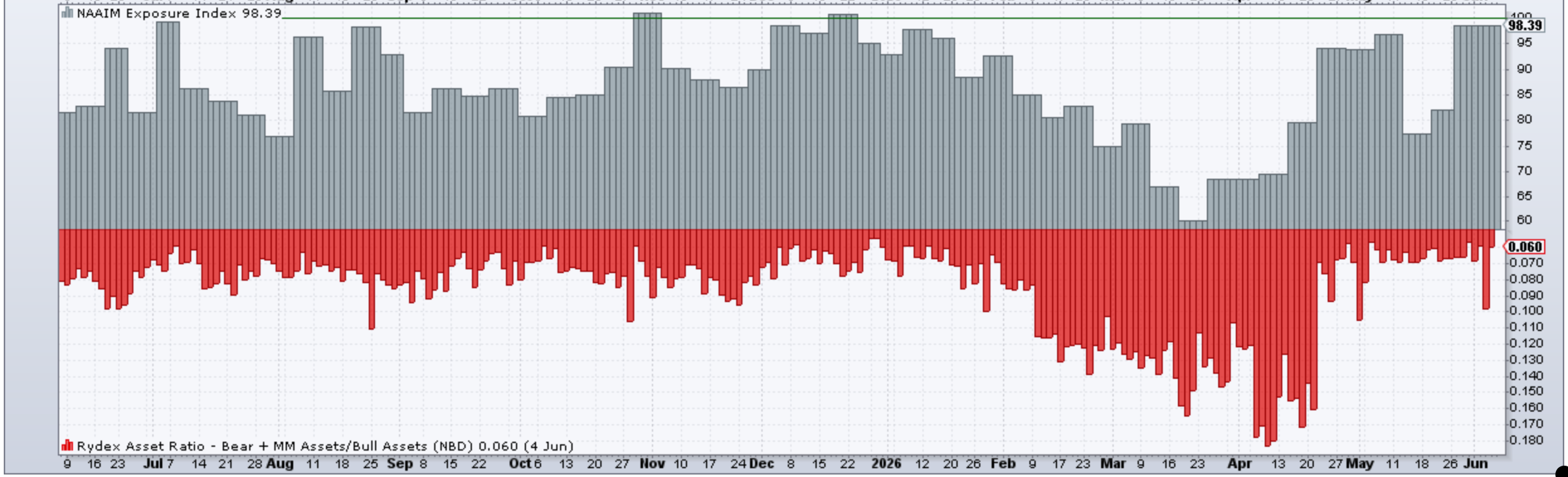

NAAIM Exposure Index is 98.39 from 68.36 at the end of March. Interesting. Note it did get into the low 30’s in April 2025 (!)

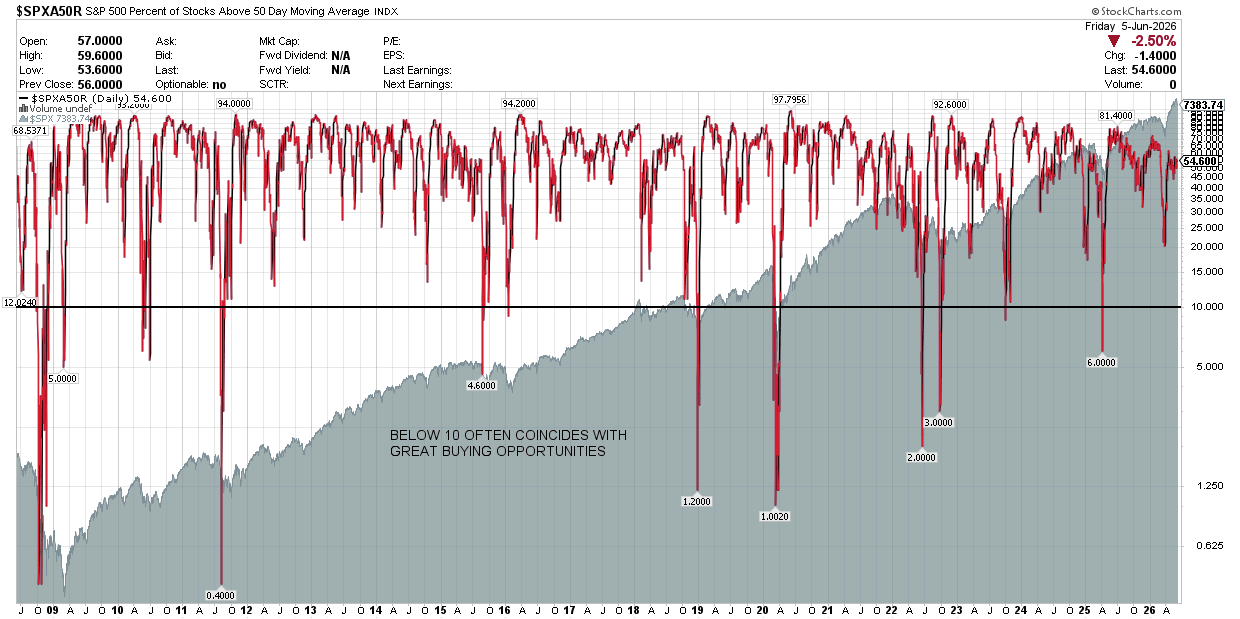

S&P 500 Percentage of Stocks Above the 50 Day Moving Average: 54.6% (<10 tend to be great buying opportunities)

Fear and Greed Index (CNN) currently reads 42 which is in the ‘Fear’ zone. At the end of March it was 19 supposedly in the ‘Extreme Fear’ zone.

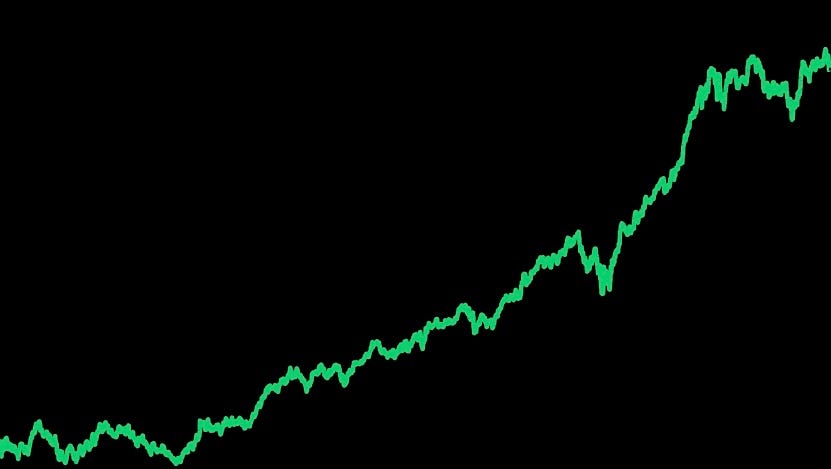

Consolidated Performance across Investment Account: YTD and since Inception of SixSigmaCapital (Equities only as of Friday 5th June)

2023: +94%

2024: +61%

2025: +57%

2026: +11.63% (with trading account gains it would be +19.53%)

TWR since Inception of SixSigmaCapital is thus +447.40% or a just over a 5.4x of the portfolio. The CAGR is 64%

TWR +4474% vs S&P 101.8%

TWR of S&P 500 in the same period is +101.81% or a 2.01x return.

SixSigmaCapital has achieved a +345.6% outperformance in that time period.

I remain pleased overall, as risk adjusted these results are very sound. Furthermore, all moves were disclosed in real time.

Equity curve since switching to my current brokerage in the last few years is below:

SixSigmaCapital Trading Account:

At the start of the year, I opened a dedicated trading account for active strategies. It was initially approximately 10% the size of my primary investment account, though has grown somewhat since then (now around 17% the size of the main book). The account is managed with a trading mindset and consists mostly of common shares, though I have utilised select options strategies.

The past month was a strong one with some needle moving trades in ARM, ASTS, FLY, OUST, USAR plus a couple of successful options trades. Of course there was several small losses and small wins also. The account progressed to +79% as of Friday 5th June.

Trading Account YTD: +79% YTD

If combined to the investment account, it would add 7.9% to the total performance.

Featured Quote:

“It’s not whether you’re right or wrong that’s important, but how much money you make when you are right and how much you lose when you are wrong.” Stanley Druckenmiller

Current Positions in Size Order with Cost Basis (Investment Account) as of June 5 2026