Ouster, Inc. (OUST)

Digital Architecture and the Battle for the Physical AI Layer

Below is a snapshot look at a name I have been trading that I think could be an interesting one to have on your radar.

The autonomous systems revolution relies on machines being able to perceive their surroundings in real time. Within this space, Ouster ($OUST) has emerged as one of the most compelling, high-beta pure plays supplying the high-resolution 3D vision required for "Physical AI."

Overview:

Ouster operates as a leading provider of high-resolution digital LiDAR sensors, which provide three-dimensional vision to machines. The company designs hardware and software that allow robots, autonomous vehicles, and smart city infrastructure to navigate the physical world safely.

Founded in 2015 by Angus Pacala and Mark Frichtl, Ouster entered the market to solve a fundamental problem: legacy LiDAR (Light Detection and Ranging) systems were too heavy, too fragile, and far too expensive. Early mechanical LiDAR units were built like spinning, analog turntables with hundreds of discrete components prone to breaking.

Ouster’s historical breakthrough was the complete digitalisation of the hardware. The company patented a system that consolidated hundreds of delicate lasers and detectors onto a single, specialised silicon microchip (using complementary metal-oxide-semiconductor, or CMOS, technology). In 2023, Ouster executed a massive merger with its primary competitor, Velodyne, cementing its status as an industry giant and inheriting a vast, defensive patent library.

Business Model: Hardware Scaling into Software Recurring Revenue

Ouster makes money through a dual-revenue mechanism.

First, it sells its high-resolution digital LiDAR sensors and camera-integrated units directly to commercial buyers across four primary industries:

Industrial automation,

Smart infrastructure,

Robotics,

Automotive.

Second, the company is aggressively expanding its high-margin software-as-a-service (SaaS) layer.

Platforms like Ouster Gemini and BlueCity add a layer of physical intelligence to the hardware, allowing traffic intersection trackers, port operators, and automated warehouse systems to monitor and analyse 3D space. This software model boosts customer retention and creates high-margin, recurring software renewal streams.

The Moat and Competitive Advantages

Ouster’s moat is built on superior unit economics and regulatory barriers rather than hardware specifications alone. By combining advanced LiDAR, camera vision, and a scalable REV8 rollout, the company is uniquely positioned to capture a massive share of the multi-billion-dollar Physical AI market.

The Digital Margin Moat: Because Ouster’s architecture relies on a single silicon chip, its manufacturing cost scales downward alongside traditional semiconductor curves. This structural design allowed Ouster to expand its GAAP gross margin to 43%, much superior to it’s analog-heavy competitors.

Extreme Diversification: Unlike many of its peers whose entire futures are tied to the slow, brutal timelines of automotive contracts, Ouster serves approximately 900 active commercial customers. This breadth cushions the company against macro downturns in any single industry.

Defense and Sovereign Backing: Ouster operates with zero debt and has achieved strict U.S. military and Department of Defense validation for its key sensory hardware. As a 100% American-headquartered entity, it stands out as a protected alternative to foreign hardware as cybersecurity and national security concerns peak.

REV 8 sensor launch in May:

REV8 is the world's first native colour LiDAR and thus represents a paradigm shift in AI perception. To perceive the world in full context, AI requires a combination of structure and colour. REV8 is the first sensor to unify both, delivering 48-bit 4K RGB colour and 3D depth data on a single piece of silicon. Also enables new applications like high-altitude drone surveying and enhanced industrial safety.

REV8 is designed for functional safety and mass-market adoption, with early traction from over 20 leading technology companies, including Google and Volvo Autonomous Solutions.

NVIDIA Collaboration: Strategic integration of REV8 with the NVIDIA Jetson platform strengthens Ouster’s software ecosystem.

Significant expansion of manufacturing capabilities by partnering with Benchmark Electronics to scale production of the Rev8 digital lidar sensor family. This partnership scales low-cost 3D sensor manufacturing to meet rising industrial and robotics demand.

Stereolabs Integration: Expands Ouster’s portfolio into AI camera vision (e.g., ZED X Nano), capturing strong demand from robotics and foundational AI developers.

Core Strategy: By combining advanced LiDAR, camera vision, and a scalable REV8 rollout, Ouster is positioned to capture a massive share of the multi-billion-dollar Physical AI market.

The Competitors and the Bear Case

Ouster operates in a highly aggressive, crowded ecosystem. Its chief international rival is Hesai Group, a massive Chinese manufacturing heavyweight that has captured dominant market share in lower-level automotive driver-assistance systems through extreme cost leadership. On the high-end automotive front, players like Luminar and Innoviz have secured multi-billion-dollar series production books directly with global luxury automakers.

The bear case for Ouster centres heavily on execution risk and near-term profitability. While peers have clear backlog visibility from automotive “whale” contracts, Ouster’s shorter-cycle, diversified purchase orders provide very little multi-year revenue visibility.

Furthermore, because commercial hardware deployments can take months or even years to scale, the company’s financial performance remains choppy. The risk of customer delays can quickly turn a profitable quarter back into a heavy operating drain.

Management

Under the leadership of Co-founder and CEO Angus Pacala, the firm remains focused on capital discipline. Unlike other tech executives who pursued consumer-facing automotive contracts at all costs, Pacala’s team pivoted into higher-margin industrial, logistics, and port automation verticals and has been noted by Wall Street for protecting cash reserves.

Fundamentals and Valuation

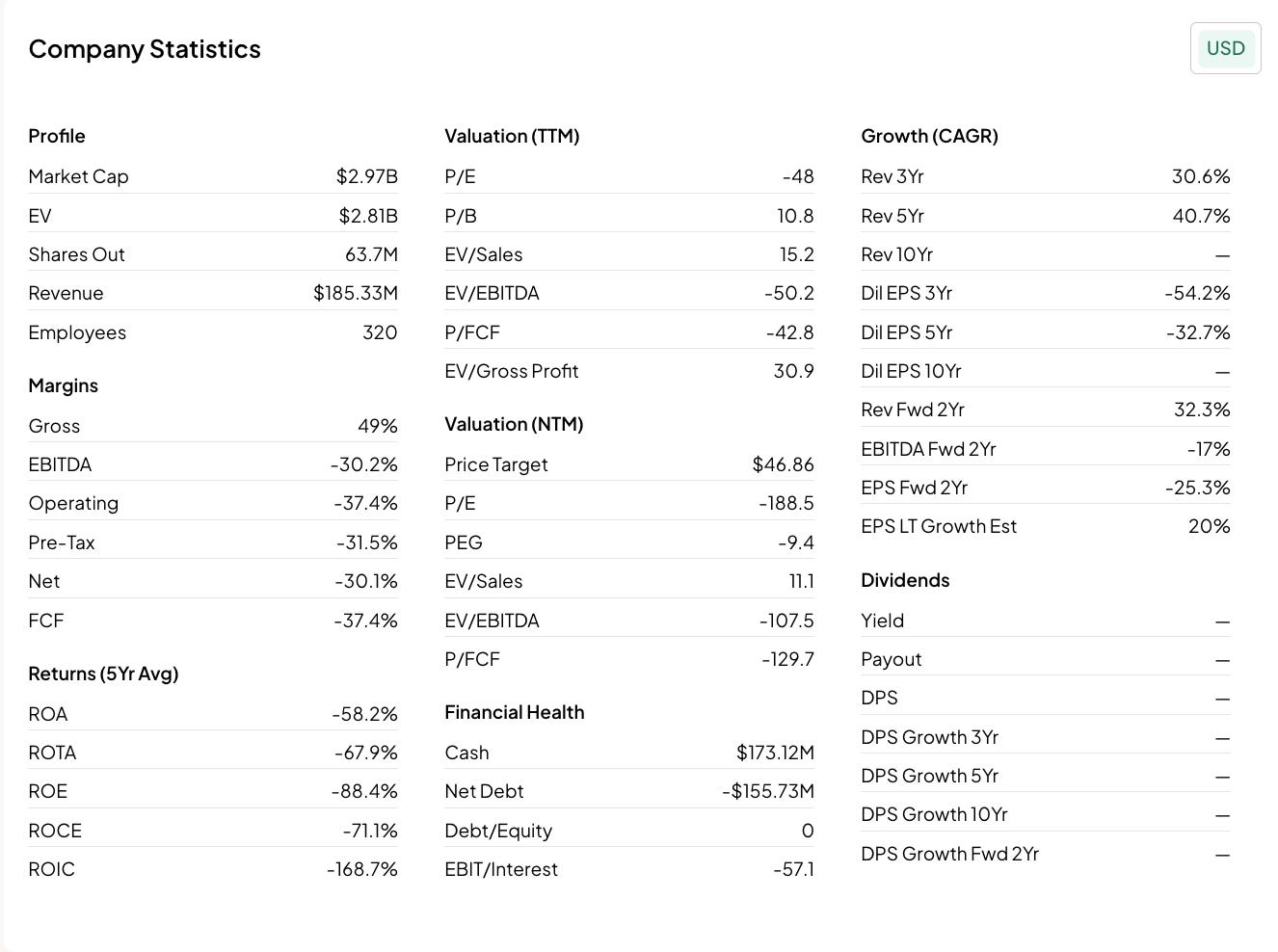

At the time of writing, OUST has a Market Cap of $2.97B with a Net Cash position of >$155M. Debt to Equity ratio is is 0.

All financials were taken from Fiscal AI’s website. You can access a free trial of the premium offering via the following link, no card required. Fiscal AI

TTM Performance:

Revenue TTM: $185.330 (M)

Gross Profit TTM: $90.791 (M)

Operating Income TTM: -$69.381 (M)

Net Income TTM: -$55.825 (M)

Valuation

OUST trades at:

15.2x LTM EV/S and 11.9x NTM EV/S.

-50.2x LTM EV/EBITDA and -95.7x NTM EV/EBITDA

-48x LTM PE and-134x NTM PE.

-42.8x trailing P/FCF and -132.7x NTM P/FCF

OUST is by no means a cheap stock and remains unprofitable. In fact, analysts expect OUST to only become profitable in FY28 For example, in its most recent quarter, Ouster reported a net loss of $17.5 million ($0.28 loss per share), missing consensus analyst estimates by a significant margin.

Long-Term Financial Framework

Management is targeting the following long-term metrics:

Annual Revenue Growth: 30% to 50%

GAAP Gross Margins: 35% to 40%

GAAP OpEx Growth: 5% to 8% capped from 2025 levels

Backed by strict capital discipline, management expressed confidence that this framework will drive positive operating free cash flow, aiming to achieve full net profitability “somewhere within 2027.”

Chart and Technicals

Currently trades at $46.57, 40.74% above the 50SMA and 73.55% above the 200SMA.

RSI 45.28

99.27% YTD

OUST is in a well defined uptrend above all moving averages. It has been respecting the 21 day moving average, so a shallow pullback to the 21 day (40.25) may offer an entry point.

Current position and plans

I own a 7% position in my trading account at an average cost of $30.20, and have already taken some profits at $48.00. I do not own it in my investing account yet. I am continuing to research this space heavily and will alert you all if I decide to add it to my long-term portfolio. However, given the nature of the asset I am more likely to keep it in my trading account as I can be more nimble.

Disclaimer: This post was for informational purposes only and does not constitute financial advice. Please conduct your own due diligence before purchasing any equities or assets discussed herein.

Thank you for reading and if you enjoyed this post, please leave a like and Restack.

Subscribe to the plan that best suits your needs and will see you in the next one!

10 times revenue and they don’t “make money”. They burn $.

Maybe Ouster is going to act like Fastly (FSLY) by having another pullback soon.

Fastly was the most similar chart I was able to find, which is down by more than -50% over the last 5 years, but up by over +100% over the last year.