Sea Limited Earnings Update: A quick look

Today, Sea Limited ($SE) released its financial report for the fiscal fourth quarter ended December 31, 2025. My long-term thesis remains on track as $SE continues to demonstrate profitable growth at scale. However, it was far from a perfect quarter; we will take a closer look below.

Full disclosure: I am currently long SE.

Overview:

Sea Limited’s 2025 was defined by record revenue and a significant leap in profitability. This performance reflects a well-executed strategy focused on operational excellence and a scaled expansion of its user base across e-commerce, digital finance, and gaming.

They successfully enhanced monetisation within Shopee through improved advertising and logistics, while SeaMoney expanded its credit offerings and refined risk underwriting using advanced AI. Garena sustained growth by delivering high-impact gaming experiences, successful IP collaborations, and a robust esports ecosystem.

This robust growth results from strategic investments in user experience, technological advancements, and disciplined financial management, allowing for both scale and profitability.

Stock Price, News & Analysis")

Key Financial Highlights

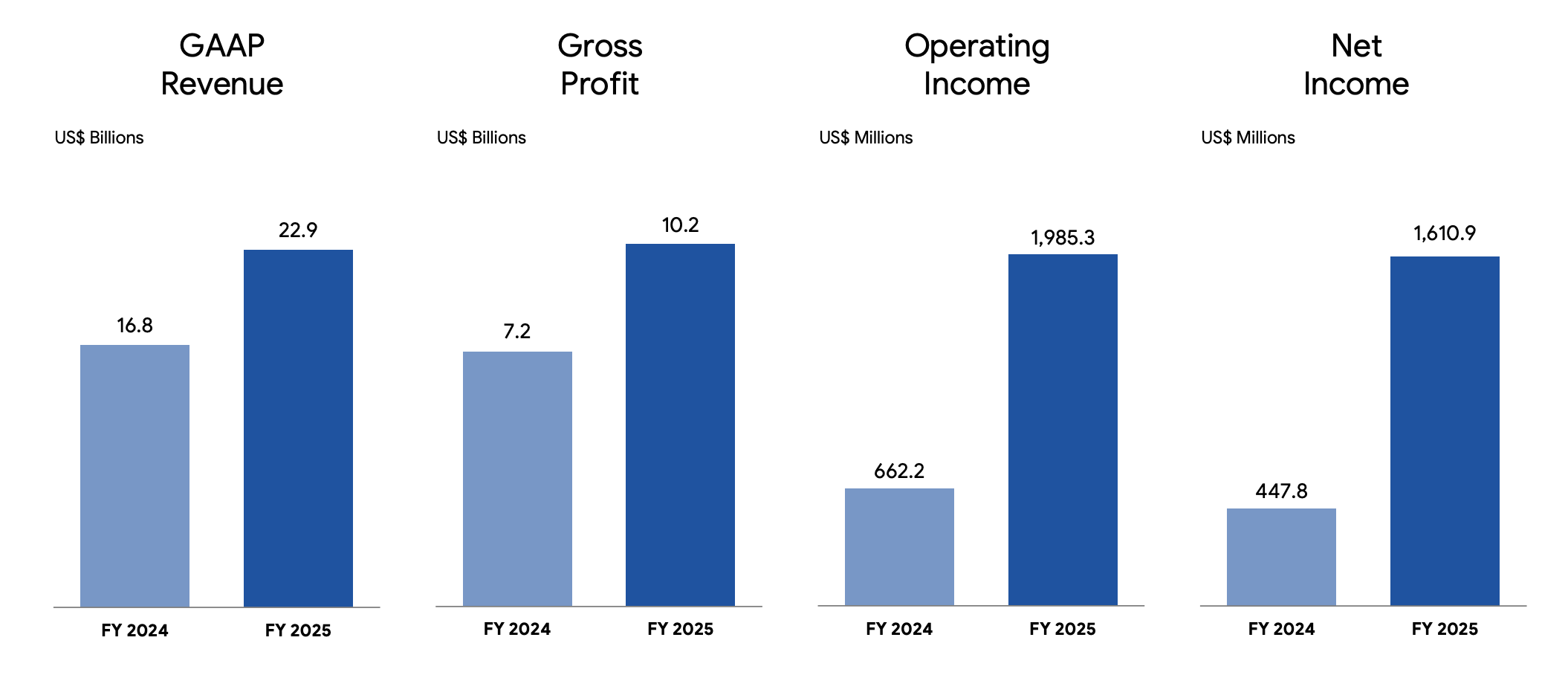

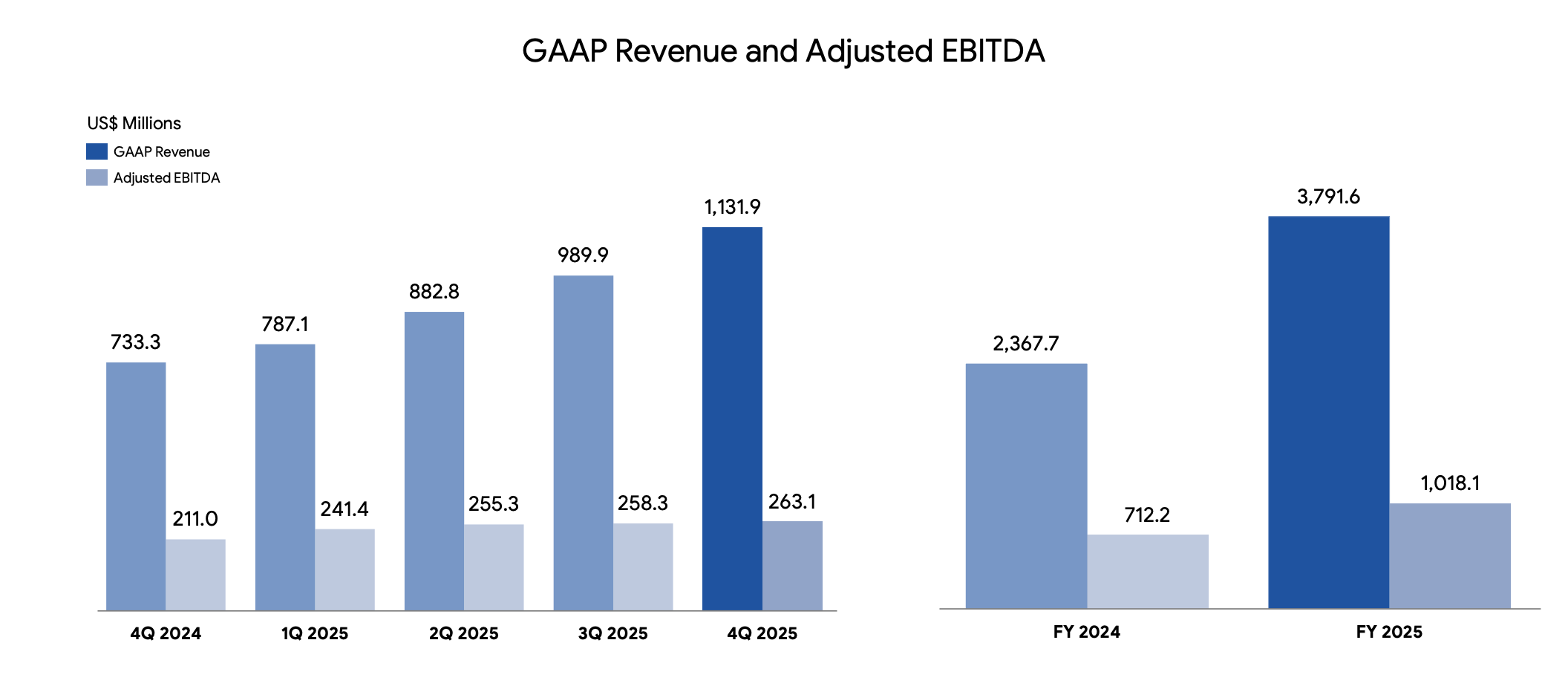

Total Revenue: $22.9 billion for full year 2025, up 36% year-on-year.

Q4 2025 revenue was $6.9 billion, up 38% year-on-year.

Net Income: $1.6 billion for full year 2025, up 260% year-on-year.

Q4 2025 net income was $411 million, up 73% year-on-year.

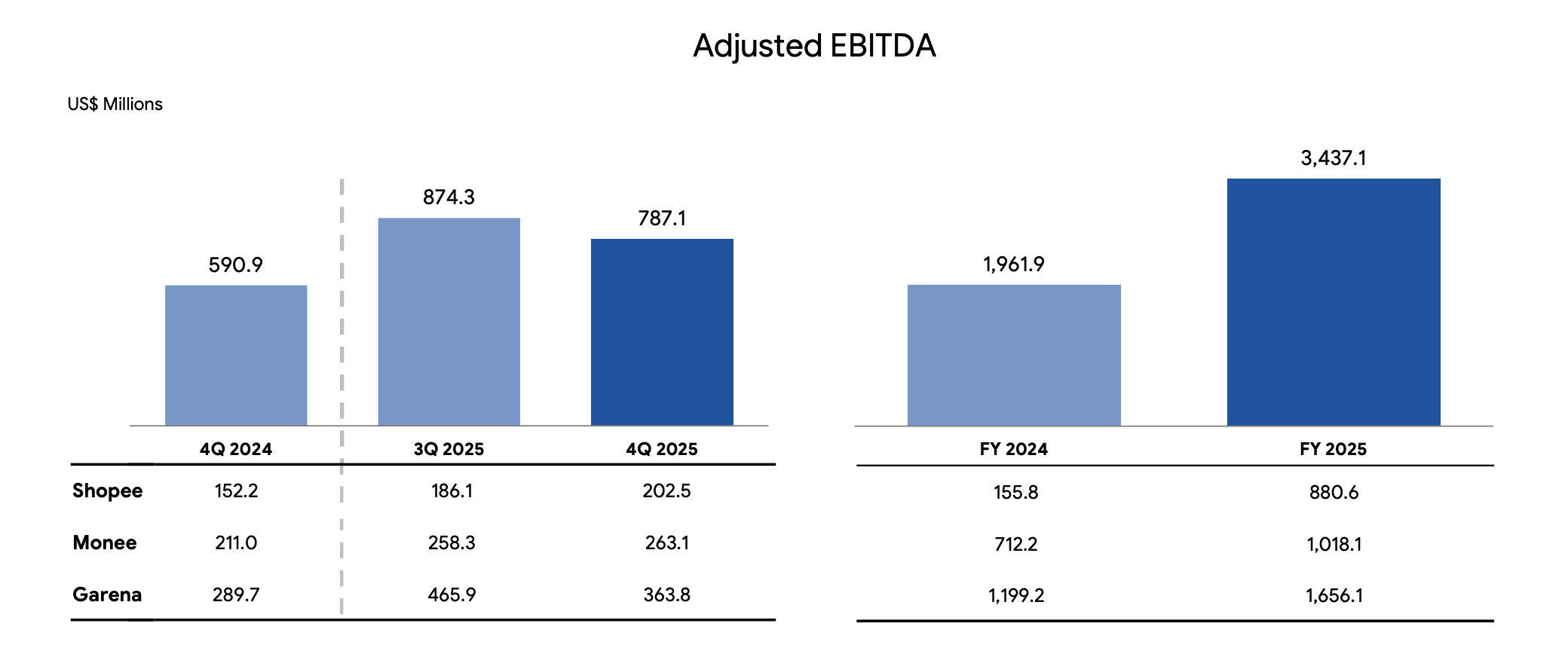

Adjusted EBITDA: $3.4 billion for full year 2025, up 75% year-on-year.

Q4 2025 Adjusted EBITDA was $787 million, up 33% year-on-year (but down Q/Q)

Shopee GMV: $127 billion for full year 2025, up 27% year-on-year.

Q4 2025 GMV was $36.7 billion, up 29% year-on-year.

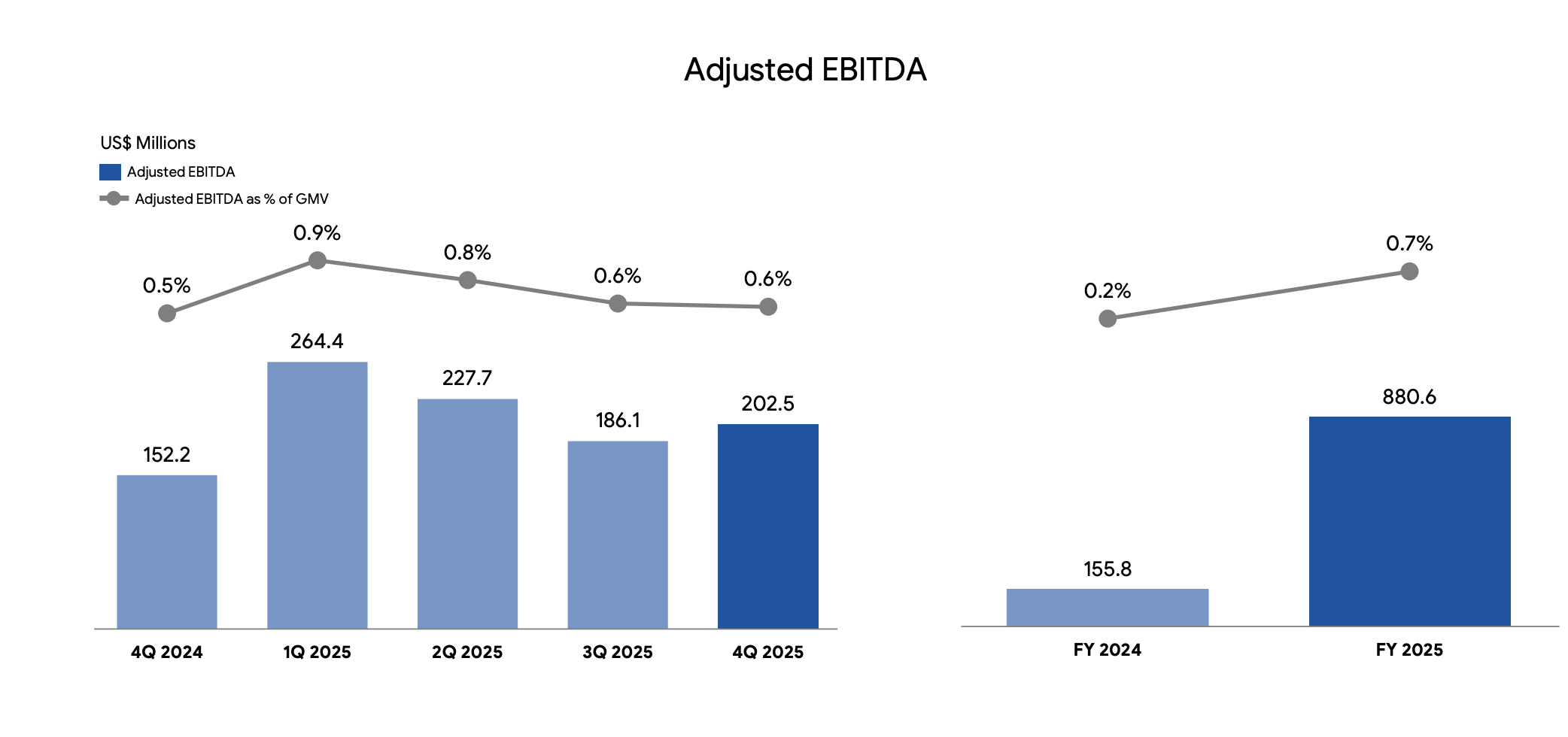

Shopee Adjusted EBITDA: $881 million for full year 2025, a significant increase from $156 million in 2024.

Q4 2025 Adjusted EBITDA was $202 million, up 33% year-on-year.

SeaMoney Revenue: $3.8 billion for full year 2025, up 60% year-on-year.

Q4 2025 revenue was $1.1 billion, up 54% year-on-year.

SeaMoney Adjusted EBITDA: $1 billion for full year 2025, up 43% year-on-year.

Q4 2025 Adjusted EBITDA was $263 million, up 25% year-on-year.

SeaMoney Loan Book: Consumer and SME loans principal outstanding reached $9.2 billion by end of 2025, up 80% year-on-year.

90-day NPL Ratio (SeaMoney): Held steady at 1.1% as of end of Q4 2025.

Garena Bookings: $2.9 billion for full year 2025, up 37% year-on-year.

Q4 2025 bookings were $672 million, up 24% year-on-year.

Garena Adjusted EBITDA: $1.7 billion for full year 2025, up 38% year-on-year.

Q4 2025 Adjusted EBITDA was $364 million, up 26% year-on-year.

Key Takeaways

Shopee:

Shopee’s strategic emphasis on logistics has become a critical differentiator, with SPX Express now processing over 30 million parcels daily and the expansion of instant and same-day delivery services leading to a 15% increase in average spending by adopting buyers. Logistics is a key area for management who recently said: “Our next goal to further deepen our logistics competitive moat is to enhance our fulfillment capability”

The Shopee VIP membership program, now rolled out across all Asian markets has over 7 million subscribers (from 2M in Q2), consistently translating to a double-digit spending uplift. In some markets, VIP members already contributed > 15% of total GMV in 4Q 2025 and members in Indonesia for example spend 30-40% more after joining.

Monetisation efforts have also been highly effective, In Q4 2025, ad revenue grew by >70% YoY and ad take rate increased by > 80bps YoY. This demonstrates Shopee’s ability to enhance profitability while driving GMV growth.

SeaMoney:

SeaMoney’scredit business experienced robust expansion by shifting to a broader “all-can-apply” approach, adding 5.8 million unique first-time borrowers in Q4 and growing active credit users to over 37 million. Off-Shopee SPayLater loans surged >300% YoY, now comprising >15% of the portfolio and ~30% usage in Malaysia. Integration with national QR systems and AI-risk underwriting drove this growth while maintaining a stable 1.1% NPL ratio.

Garena:

Garena saw a blockbuster year, with Free Fire exceeding 30% bookings growth for two years, driven by IP collaborations (Naruto, Squid Game) and a world-record-setting esports ecosystem. Successful launches like EA Sports FC Mobile in Vietnam further diversified the portfolio, proving Garena’s ability to effectively localise and engage global franchises.

Guidance

For 2026, Sea Limited anticipates continued strong growth and healthy profitability across its segments.

Shopee is projected to grow its annual GMV by approximately 25% year-on-year, with “its full-year Adjusted EBITDA expected to be no lower than 2025 in absolute dollar terms” reflecting a strategic choice to prioritise growth while upholding financial discipline. (IMO, the quote in bold is the main reason the stock sold off today!)

Garena is forecasted to achieve double-digit bookings growth for 2026, with plans for further IP collaborations and football-related promotions.

SeaMoney is expected to continue its strong growth trajectory, with significant long-term profit contribution potential as initiatives mature and expand beyond credit into digital banking and insurance.

The company maintains its belief in achieving a 2-3% EBITDA margin for its e-commerce business in the medium to long term.

So why did it sell off?

In my view it comes down to the 3 following things:

The quote below implies that EBITDA margins will regress despite increased revenue: ‘For 2026, we aim to grow Shopee’s annual GMV by around 25% YoY, with its full-year adjusted EBITDA no lower than that of 2025 in absolute dollar terms.’ To me, this suggests a strategic choice to prioritize growth. While this may be the correct move for the long term, it will likely act as a hangover for the stock until margins inflect upward again. For reference, adjusted e-commerce margins peaked at 0.9% in Q1 2025 but have been trending lower ever since.

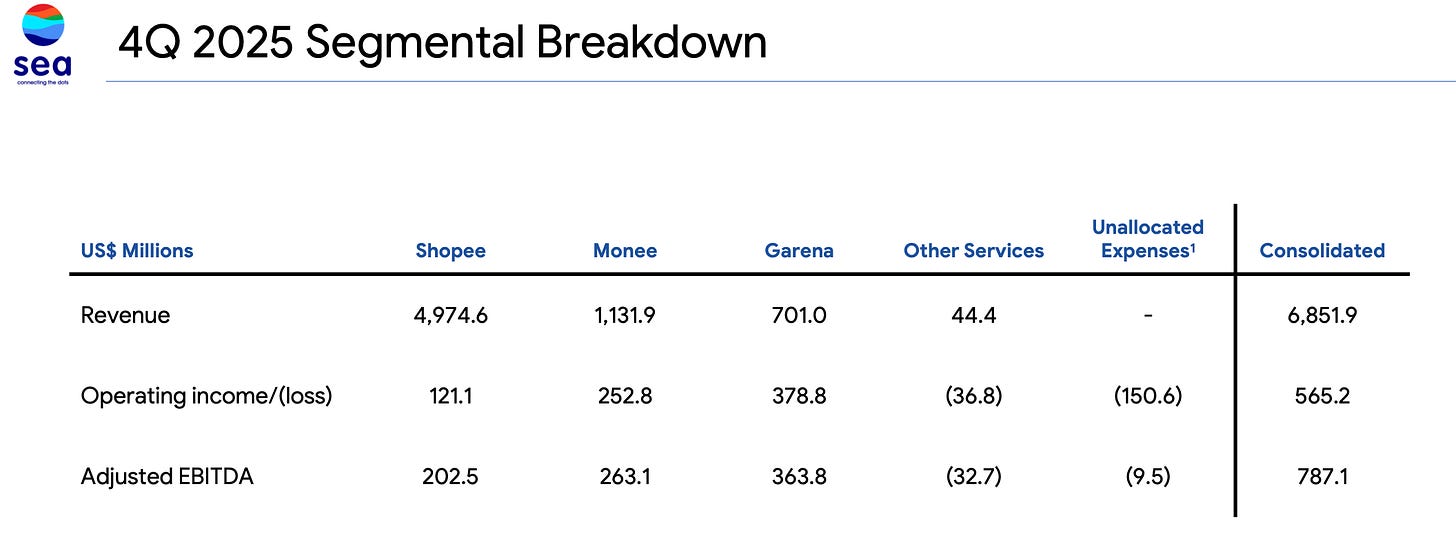

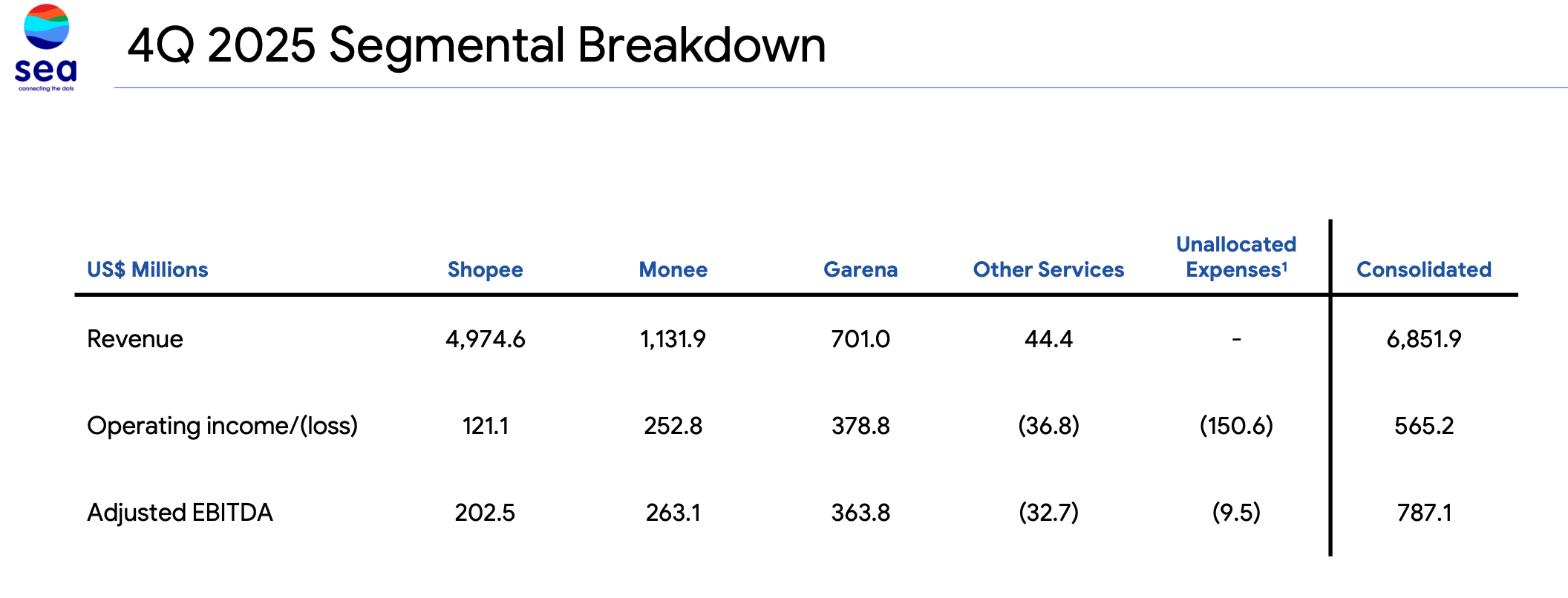

In the SeaMoney (Monee) segment, while the loan book grew by over 80% to $9.2 billion and revenue surged 54.3%, adjusted EBITDA grew by only 24.7%. This lag was primarily due to a 66.7% increase in provisions for credit losses. Investors may be concerned that the company is expanding its loan book too aggressively at the expense of credit quality.

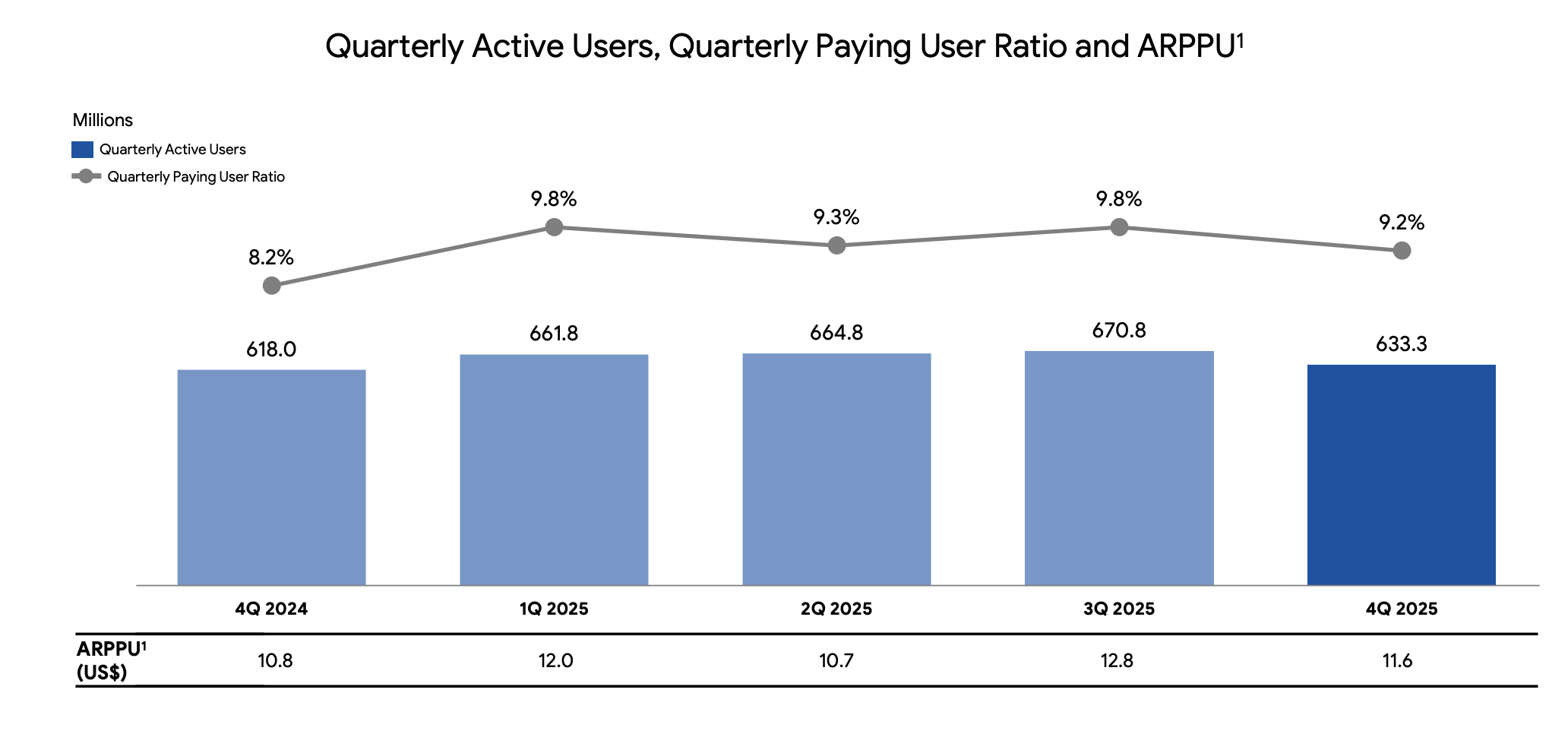

In the Garena segment, first-glance results were solid, with bookings up 23.8% and adjusted EBITDA up 25.5%, reflecting slight margin expansion. However, while users grew year-over-year, they actually declined on a quarter-over-quarter basis, as did bookings. Furthermore, both the quarterly paying ratio and ARPU fell QoQ, suggesting a potential loss of momentum after the holiday peak.

Final thoughts:

Overall, $SE reported robust earnings with a double beat, though there were several areas of concern. Margin compression across Shopee and SeaMoney can be viewed either as a negative or through the lens of management prioritising strategic growth. While this may be the correct long-term move, it could act as a hangover for the stock until margins inflect upward again.

Similar concerns regarding declining adjusted EBITDA margins were raised during the previous call, to which management responded: ‘I think if you look at the year-to-year trend... we believe that we are able to deliver the 2%–3% EBITDA margin as we shared before.’ I want to see margins improve year-over-year moving toward that 2%–3% goal.

My thesis remains intact; I plan to hold for the long-term and will look to add one final tranche to reach my maximum 5% allocation at cost.

Access the shareholder letter below:

https://cdn.sea.com/investor/4Q2025/JcKns4LaJC8bxcQdJwXz/2026.03.03%20Sea%20Fourth%20Quarter%20and%20Full%20Year%202025%20Results.pdf

Great write up. This company really is building a franchise in ways that AI helps rather than disrupts as long as human employment remains strong, and you made me appreciate that with this summary. Technically the $77.05 at the open this morning in the ADR fits with a possible bottom.

I'm confused about these provisions everyone is talking about like it's a bad thing.

Sea has tracked provision growth about in line with loan growth, there is no massive disconnect either side. This is the proper thing to do, and normal.

Meli and it's big disconnect of much higher loan growth vs provision growth is the more suspicious one.