TransMedics Group Inc Earnings Update: A quick look

Today, TMDX submitted their Financial report for fiscal fourth quarter ending December 31. The thesis remains on track for me and I was especially impressed with growing OCS case volumes and increased clinical adoption of its National Organ Preservation (NOP) program.

Full disclosure we are currently long TMDX at an average of $66.15.

Overview:

TransMedics' strong performance in the fourth quarter and full year 2025 was primarily driven by a significant recovery from earlier seasonal challenges in U.S. transplant activities, coupled with growing OCS case volumes and increased clinical adoption of its Organ Care System (OCS) National Organ Preservation (NOP) program.

The company's integrated logistics platform, including its owned and operated aviation fleet, played a crucial role in enabling this growth by expanding the utilisation of available donor organs. This strategy has allowed TransMedics to not only gain market share but also to expand the overall U.S. liver, heart, and lung transplant market, demonstrating the transformational impact of its technology and service offering.

Key Financial Highlights:

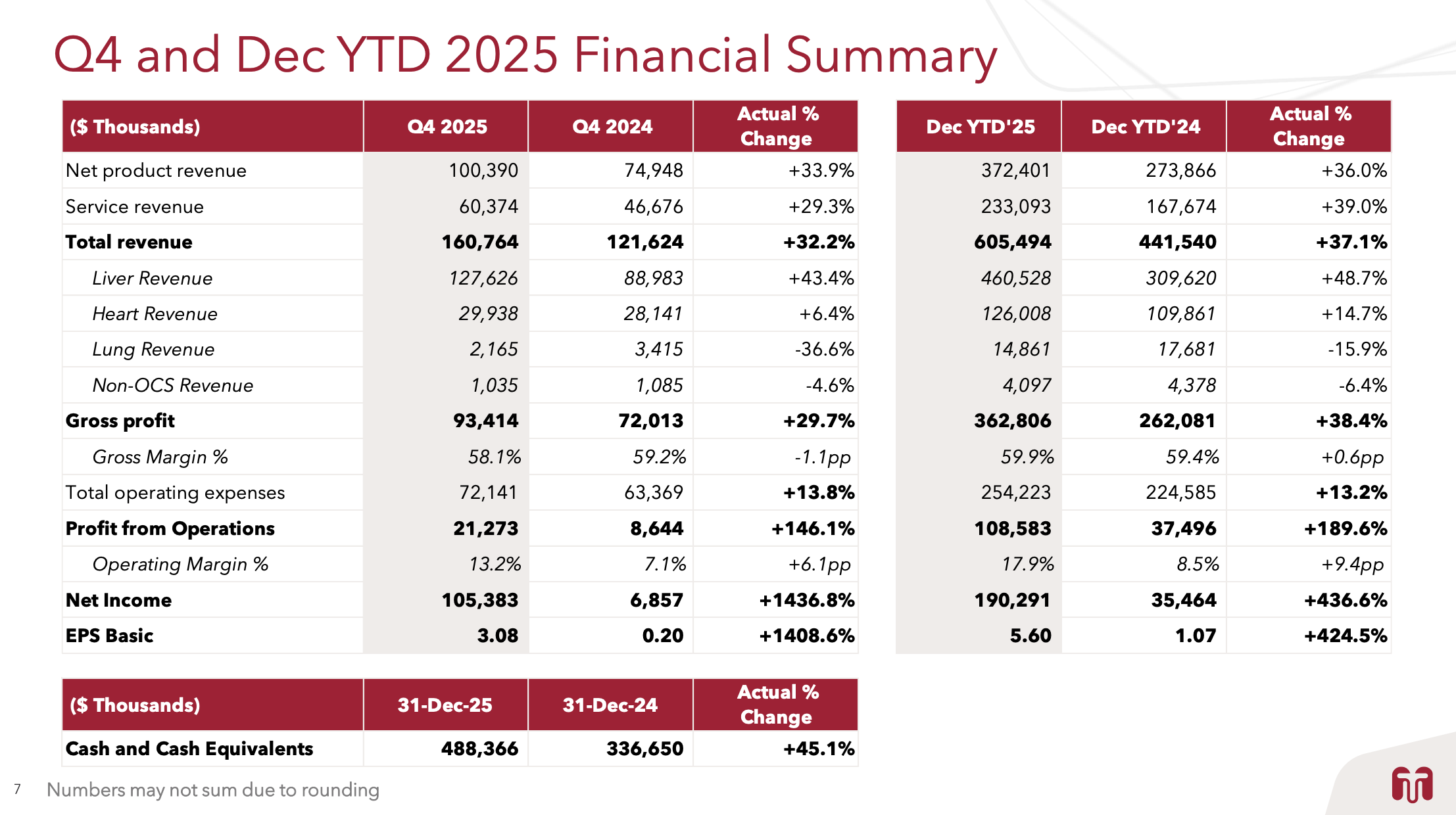

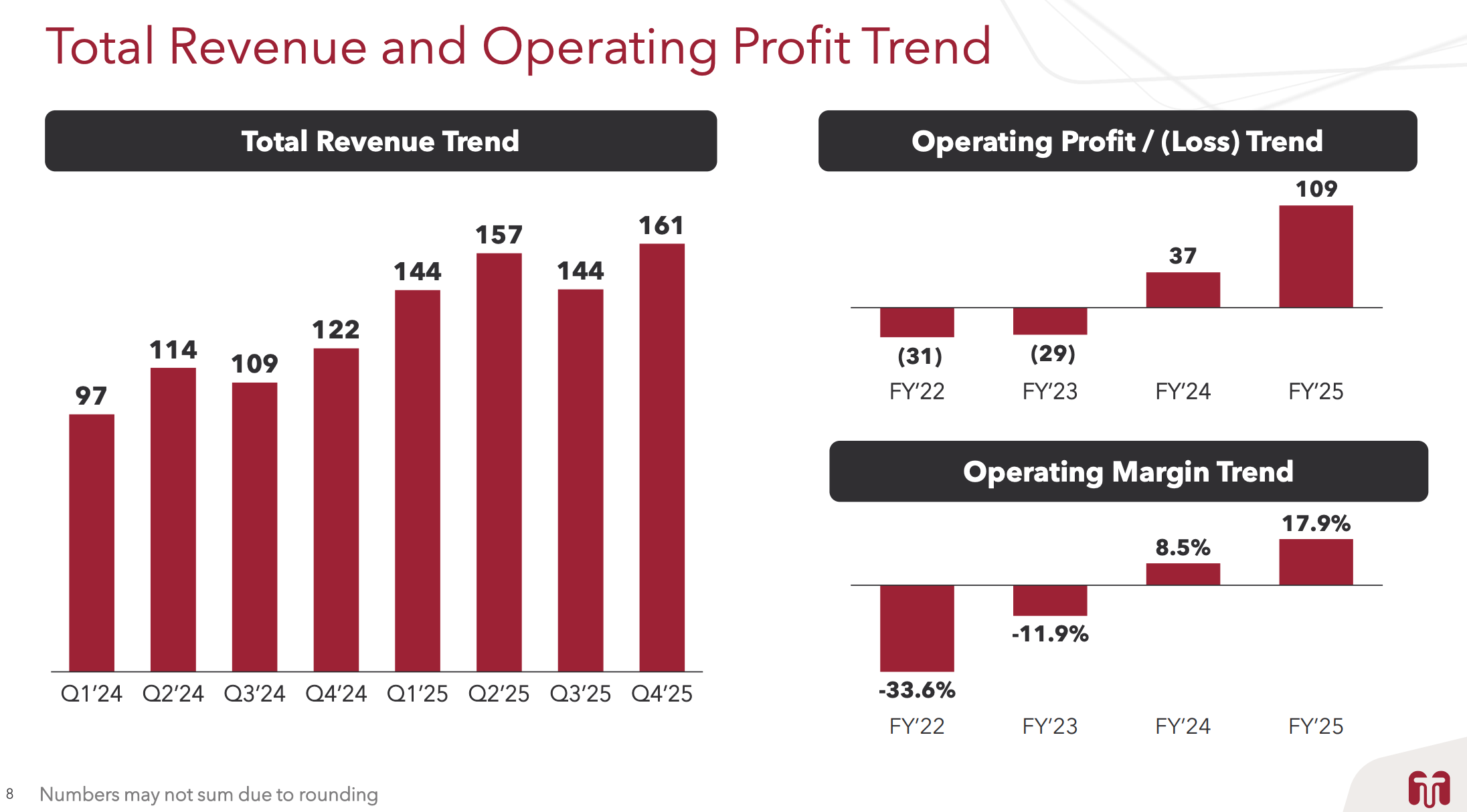

Total Revenue Q4 2025: $160.8 million, representing 32% Y/Y growth and 12% sequential growth.

Total Revenue Full Year 2025: $605.5 million, representing 37% Y/Y growth.

Gross Margin 2025: 59.9%, up from 59.4% in 2024.

Operating Profit Q4 2025: $21.3 million, or 13.2% of total revenue.

Operating Profit Full Year 2025: $108.6 million, or 18% of total revenue.

Net Income Full Year 2025: $490 million, significantly up from $36 million in 2024, includes an $83.8 million income tax benefit from the release of a valuation allowance on deferred tax assets.

Diluted Earnings Per Share 2025: $4.87.

Cash and Cash Equivalents (as of December 31, 2025): $488.4 million.

Key Takeaways:

TransMedics has played an important role in expanding the overall U.S. transplant market, rather than merely taking market share. Since 2022, U.S. national transplant volumes for liver, heart, and lung grew by 25% with OCS NOP, but would have declined by approximately 1% without OCS volume. This demonstrates the significant impact of the OCS NOP program in increasing the utilisation of donor organs.

The OCS liver program demonstrated exceptional performance (see image demonstrating Y/Y growth), with OCS liver transplants representing 36% of the overall U.S. liver transplant volume in 2025, up from 26% in 2024, driven by strong clinical outcomes and execution.

Furthermore, the NOP Connect 2.0 digital ecosystem is showing early operational efficiencies in managing cases, billing, and providing transparency.

TMDX is strategically investing in several new clinical programs and international expansion to fuel future growth.

The Enhanced Heart Program, with Part A focused on functional enhancement and Part B on demonstrating superiority over cold static storage, is a key initiative. Notably, Part B faces competitive dynamics as some cold storage providers are hesitant to participate in head-to-head comparisons, which TransMedics views as a testament to the confidence in its technology.

The De Novo Lung Program aims to reinvigorate the U.S. lung transplant market, which currently sees low OCS adoption. Both programs have received FDA clearance and are in various stages of trial activation.

Beyond the U.S., TransMedics is actively launching its NOP model in Italy and exploring other European countries, this has the potential to nearly double its TAM.

The OCS Gen 3.0 platform, a more compact and automated system, is a major long-term catalyst launching with a kidney program aimed at the high-volume U.S. transplant market. This technology is also being adapted for liver, heart, and lung systems. Furthermore, a significant $83.8 million Q4 2025 tax benefit underscores management’s confidence in the company’s sustained profitability and scalability.

Guidance:

TransMedics anticipates 2026 total revenue between $727 million and $757 million, representing 20% to 25% growth driven by OCS adoption and service expansion. Note, analysts were at 725M prior to the update. While long-term gross margins are projected at 60%, near-term pressure may arise from international investments.

Operating margins are expected to be approximately 250 basis points below 2025 levels due to transitory investments in OCS 3.0 and clinical programs, though they are projected to reach 30% by 2028. The company will maintain 22 aircraft and implement a double-shifting pilot program. Key challenges include the EU launch pace, trial timing, competition, and U.S. market seasonality.

Final thoughts:

TMDX continues to deliver quarter after quarter and is establishing the new standard of care for organ transplantation. The operating leverage at play is very impressive.

The thesis remains intact for me; I plan to hold my shares and will look to add on meaningful pullbacks.

Have you looked at SRTA?