TransMedics, Inc. Earnings Update: A quick look

Growth Intact, but Margin Erosion Takes Center Stage

Last night, TransMedics, Inc. (TMDX) released its financial report for the fiscal first quarter ending March 31. We will take a closer look below.

Overview

In my assessment, the market’s negative reaction primarily stems from a significant miss on operating expenses, which grew 42% Y/Y, far outstripping revenue growth. While the top line remains robust, management is aggressively “front-loading” investments, leading to a temporary compression in margins.

Financial Performance & Guidance

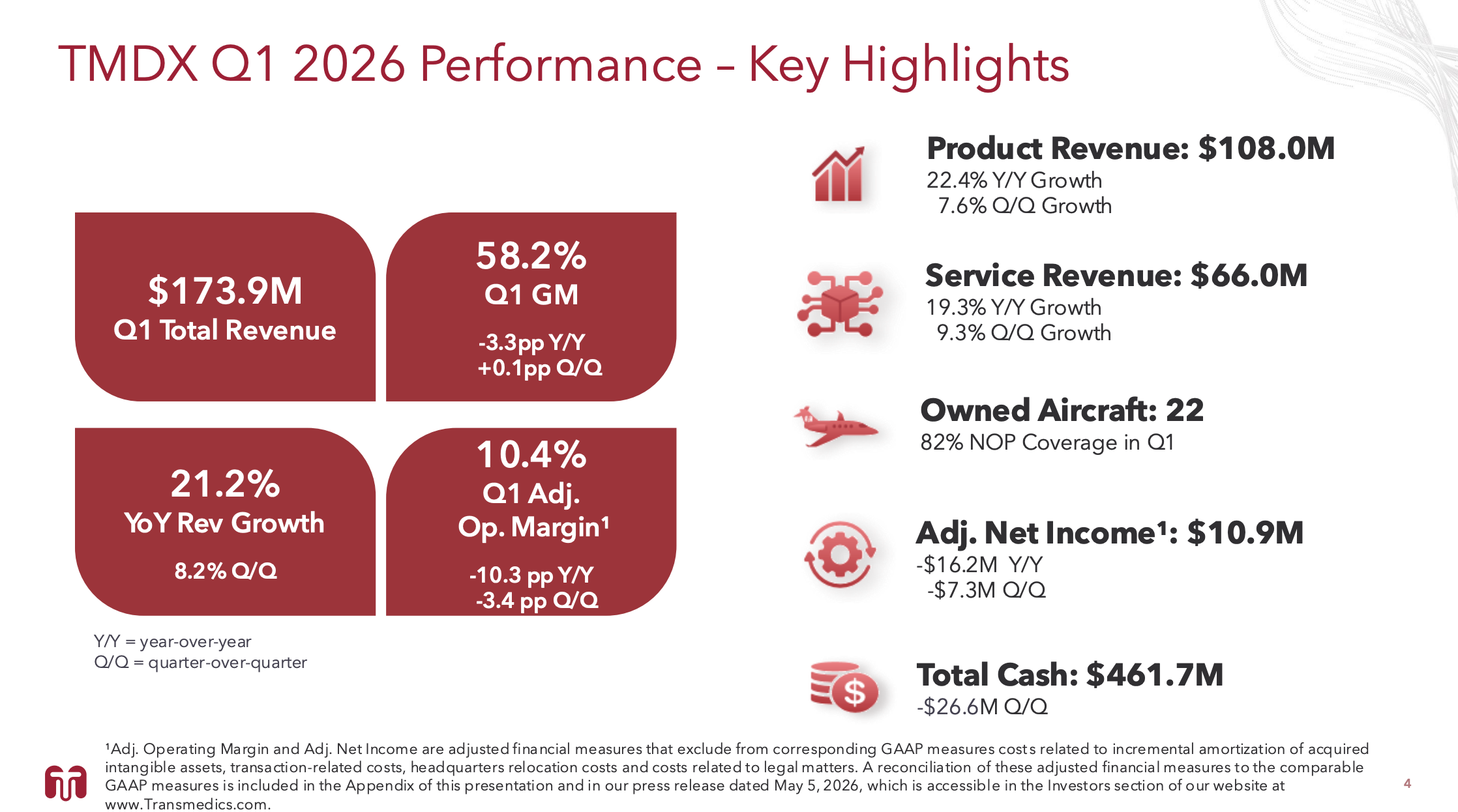

Revenue: $174M (+21% Y/Y, +8% Q/Q).

U.S. Products: $102M (+22% Y/Y).

Logistics (NOP): $32M (+22% Y/Y, +12% Q/Q).

International (OUS): $6M (+39% Y/Y). Small base but high velocity.

Margins:

Gross Margin: 58.2% (down from 61.5% Y/Y) due to supply chain and NOP expansion.

Operating Margin: 10.3% (down from 20.75% Y/Y).

The Expense Surge: Where is the Money Going?

Operating expenses rose 42% Y/Y (R&D +45%, SG&A +41%). Management is prioritising the following strategic pillars:

Growth: R&D for OCS Kidney, OCS Gen 3.0 (Liver, Heart, Lung), and European expansion.

Operational Excellence: System upgrades and talent acquisition to scale.

Infrastructure: New global headquarters and facility upgrades.

CHOPS, which is viewed as an additive acquisition.

Key Monitoring Points:

Opaque Communication: Management was vague regarding energy price impacts and the introduction of new non-GAAP measures, is this an attempt to mask GAAP earnings volatility?

Market Share: Management insists they are maintaining/growing share despite competitive noise.

Fuel Costs: Claimed to be a “small component” of flight hour costs and effectively covered.

Guidance

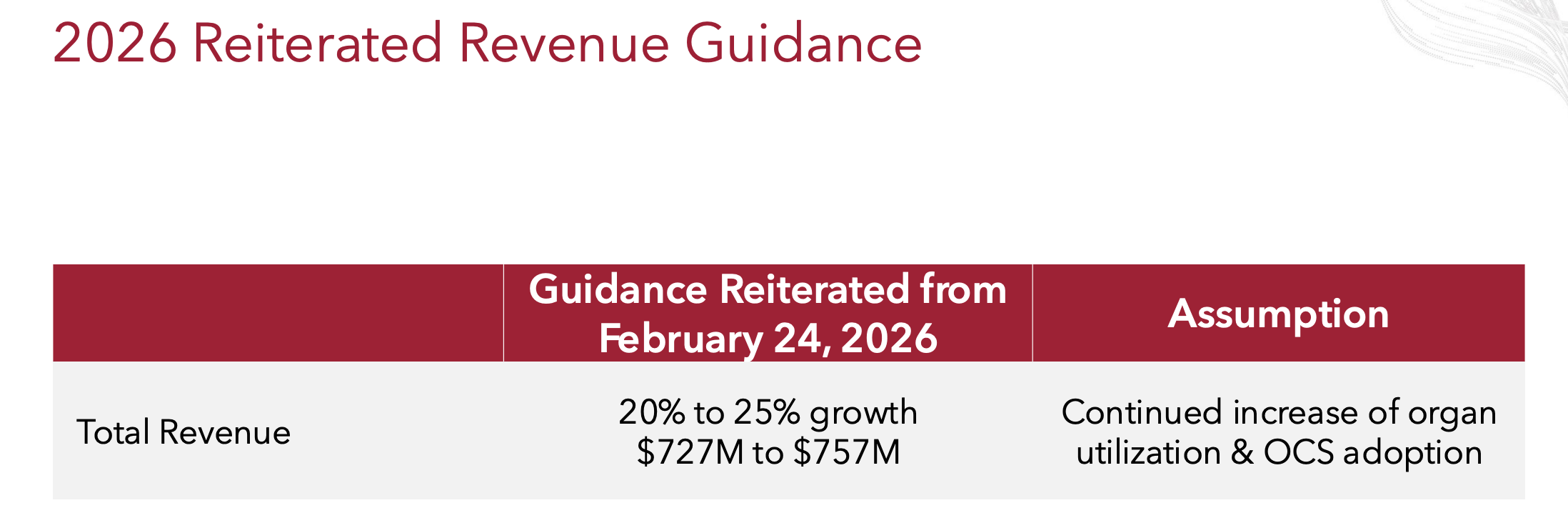

Revenue Growth: Reiterated target of $727M–$757M (up 20%–25% Y/Y). Growth drivers include higher transplant volumes via OCS/NOP platforms and international scaling.

Margin Pressure: Expect near-term gross margin compression as the company “front-loads” investments in infrastructure and global expansion.

Long-Term Goal: Aiming for a 60% gross margin as the business scales and higher-margin products (Kidney program, OCS Gen 3.0) gain traction.

Operating Margin Outlook: Expected to finish the year up to 250 basis points lower than the 2025 adjusted operating margin, reflecting the heavy upfront spending. This implies a recovery from the 10.4% seen in Q1.

Investment Thesis & Action Plan

Valuation: Based on the 15% OM guide and $740M revenue, the stock trades at approximately 24x FY26 Operating Income. This is not especially cheap, though still inexpensive for the growth profile.

Market Sentiment: The stock is likely in the ‘penalty box’ until there is tangible proof that operating expenses are under control and margins are trending back toward the 15%+ target. The operating expenses will have to be tempered for investors to rebuild confidence.

Personal Stance:

Current Position: 2% weighting leading into the print after trading around a core, now closer to a 1.5% position.

Action: Hold. No selling, no adding as it is neither excessively cheap nor showing technical recovery yet.

Strategy: Observing the “3-day rule” before considering any changes. The retail-heavy shareholder base may lead to continued selling pressure in the immediate term.

Access the First Quarter 2026 Financial Results below:

https://investors.transmedics.com/static-files/37739be5-5380-451c-ba28-31164b942161

Thank you for reading and see you for the next one!