TWST: Twist Bioscience Corp Update

TWST: Securing Profits After a Strong Stretch

Since we went long TWST last winter, shares are up more than 3x, although based on my cost basis I am up 260% as of Friday’s close on remaining shares.

I did trim some shares on June 26th for a 312% gain (see attached link to transaction log) and have covered my cost basis a couple of times over.

However, I believe the stock is becoming fully valued and somewhat overbought now, so it may be time to consider trimming. The fundamental and technical breakdown is below.

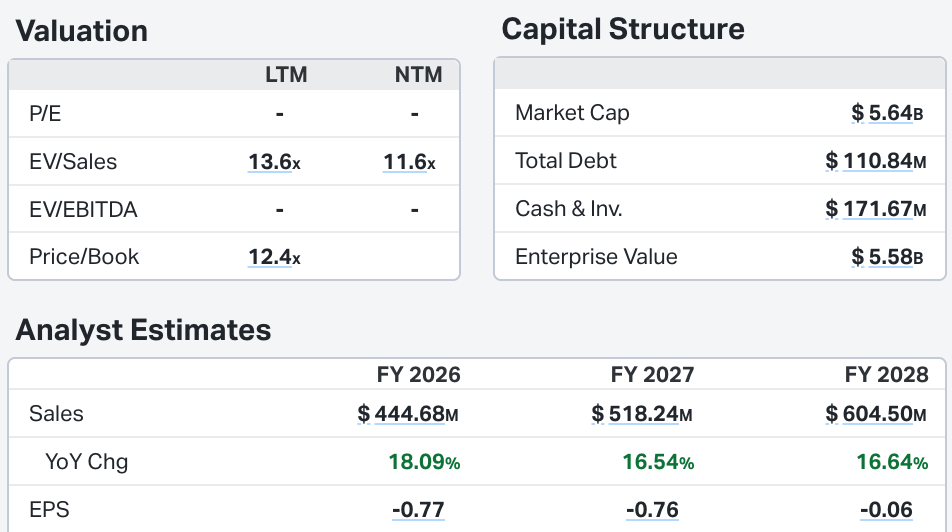

Fundamental snapshot:

The NTM EV/Sales multiple is now at 11.6x, whereas when we went long, it was trading at just 3.7 or 3.8x. This is a significant multiple expansion and not a low multiple for a company growing revenues at a mid-teens rate while remaining unprofitable as things stand.

Technicals:

Currently trades at 90.64, 24.41% above the 50SMA and 88.91% above the 200SMA.

RSI 55.73

179.82% YTD

The chart below shows that TWST is trading above all key moving averages and is in a well-defined uptrend. I have annotated the chart with my key transactions.

Whilst TWST has pulled back slightly from its ATH, it remains 89% above the 200 SMA, which is generally considered extended. Furthermore, if we see the weekly chart

Furthermore, the weekly chart shows that the stock is overbought, with the RSI recently reaching into the 80s (see arrow). We also saw notable distribution last week (see second arrow).

Taking the above into consideration, it is a prudent time to consider removing your initial cost basis or having a clear plan for taking profit such as reducing on strength or conversely on EMA 21 violation. As noted, I have already been doing just that.

Thank you for reading and see you for the next one!