Actionable Stock Set-up 11: Reddit Inc (RDDT)

Human-Curated Data: the Ultimate AI Infrastructure Play?

In this edition of Actionable Stock Set ups, we will be taking a look at the Investment Case for Reddit Inc (RDDT). It is the 11th entrant into the Actionable Set-ups series.

Layout:

Executive Summary

Overview of Reddit Inc

Bull and Bear Case

Management

Financials and Valuation

Chart

Current position and plans

This post is for informational purposes only and does not constitute financial advice. Please conduct your own due diligence before purchasing any equities or assets discussed herein.

Executive Summary

Reddit is a differentiated social media platform aiming to become the most human place on the internet. As a founder-led business in the early stages of its monetisation journey, it offers a rare combination of 90% gross margins and a massive, untapped data repository.

Currently trading at 22x forward Non-GAAP earnings, the valuation is compelling relative to an expected 29% top-line CAGR over the next five years. If Reddit achieves this growth while scaling operating margins toward 40%, the business is on a clear path to generating $3 billion in annual operating profit.

With Daily Active Users (DAUs) projected to double and high-conviction insider buying occurring as recently as February 2026, the risk-reward profile suggests significant long-term upside.

Reddit Inc operates a massive network of over 100,000 active communities (subreddits) where users engage in human-curated discussions. Unlike follower-based platforms like Instagram or X, Reddit is interest-based. On reddit you can expect to see :

Human-Generated Context: It serves as one of the internet’s largest archives of authentic, conversational human data.

Search Hub: Increasingly, users use Reddit as a search engine (e.g., adding “reddit” to Google queries) to find unbiased reviews and advice from real people. Over 80 million people were searching directly on Reddit every week in Q4, up from 60 million just one year ago.

AI Training Ground: It’s massive repository of text is used to train Large Language Models (LLMs), making it a critical infrastructure provider for the AI industry.

Reddit is positioning itself as 'the most human place on the internet'—a space where users dive into their interests and seek authentic connection. In a world flooded with AI slop, people are seeking real community, lived experience, and trusted opinions. That’s Reddit’s differentiator.

How Does Reddit make Money?

Reddit’s business model is primarily built on two pillars:

Advertising (90%+ of Revenue):

Contextual Targeting: Because users organise themselves into specific interests (e.g., r/Gaming, r/PersonalFinance), advertisers can target high-intent audiences without relying as heavily on invasive tracking. This is ideal.

AI Ad Solutions: Recently Reddit rolled out “Reddit Max,” an AI-powered automated ad system that helps small and medium businesses (SMBs) launch campaigns with better conversion rates.

Data Licensing:

This is Reddit’s high-margin growth wildcard. The company has multi-year deals with the likes of Google and OpenAI to license its plethora of human conversations for AI training. This revenue is almost pure profit since the content is user-generated. This is an important pillar.

Premium Memberships & Marketplace:

Includes Reddit Premium (ad-free browsing) and the “Contributor Program,” which allows users to earn money and Reddit to take a cut of digital gold and avatar sales.

Bull case

Reddit is transitioning from a social media site to a high-margin AI infrastructure play.

The “AI Data Firehose” (Pure Profit)

Reddit sits on 18 years of human conversation, this is arguably the highest-quality training data for LLMs.

High-Margin Revenue: Unlike ads, data licensing has almost zero cost of goods sold. Deals with Google and OpenAI are just the beginning; as AI models require more authentic human data to avoid collapse of the models, Reddit’s pricing power increases. Or in theory it should!

The Flywheel: Every new community interaction is a fresh data point to sell.

Massive Operating Leverage

Reddit’s financials in early 2026 show a business that is scaling profitably.

90%+ Gross Margins: Reddit has some of the highest gross margins in the tech sector.

Profitability Pivot: Reddit turned a $530 million net profit in 2025.

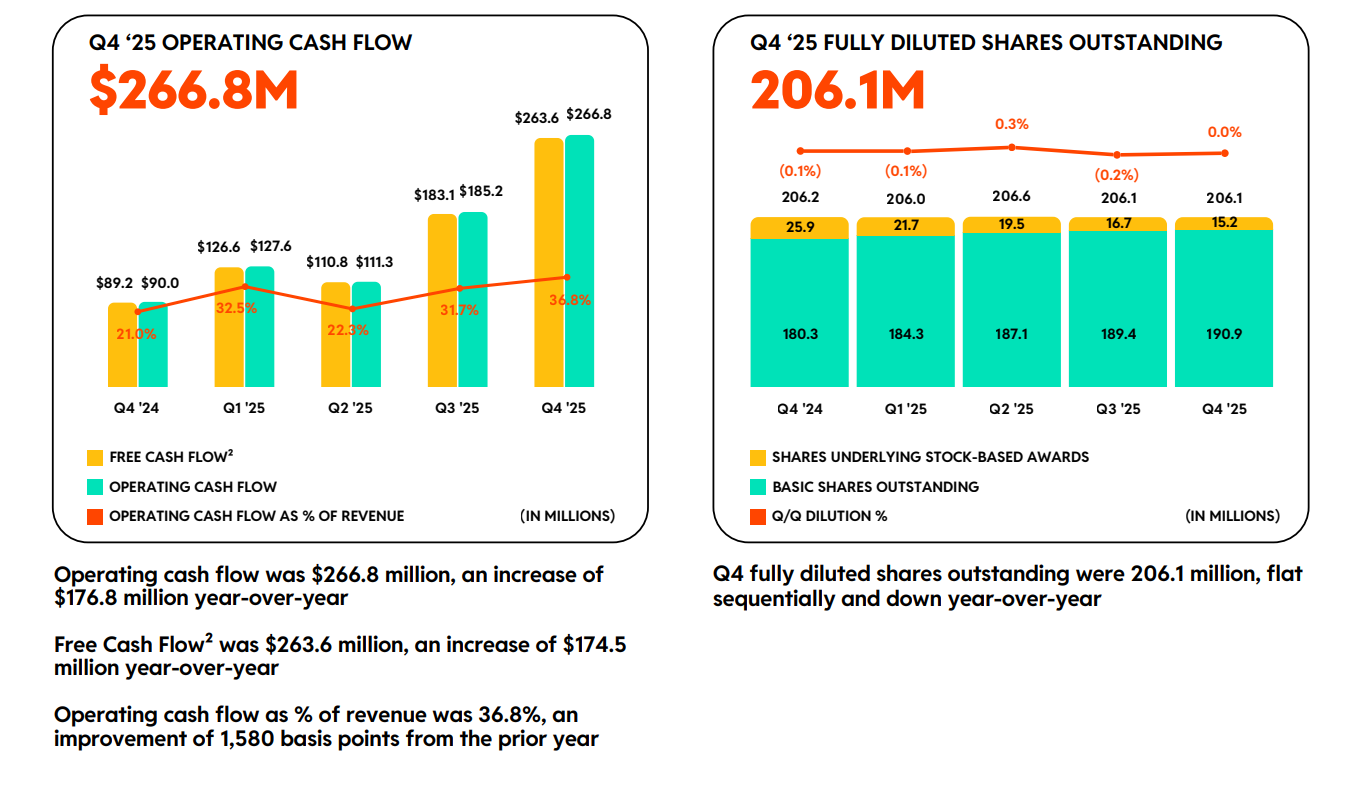

Buyback Signal: While the $1 billion share repurchase announced in February 2026 demonstrates a commitment to returning capital, investors shouldn't overlook that the program is in part to counter-act ongoing dilution from stock-based compensation.

Untapped International Potential

Reddit has historically been very US-centric, but AI is changing that.

AI Translation: Using machine translation, Reddit has opened its subreddits to 30+ languages. This allows a user in France to read and contribute to a US-based community in real-time, instantly expanding the Daily Active User (DAU) ceiling without needing to build local versions of the site. AI is driving efficiency in the business.

Improving Ad Efficiency (ARPU Growth)

Reddit Max is making Ads more efficient.

AI-Driven Ads: Their new automated ad platform has shown conversion improvements of up to 27%.

ARPU Expansion: In Q4 2025, Average Revenue Per User (ARPU) jumped 42% YoY to $5.98. There is still a massive gap between Reddit’s ARPU and Meta’s, representing a runway for growth, though matching META’s ARPU is a tough ask. The chart below shows Global ARPU and ARPU by region.

The Search Engine Displacement?

Besides LLM’s, more and more users are flocking to Reddit for authentic answers.

Reddit Answers: By integrating AI-curated summaries of community discussions directly into the app, Reddit is becoming a primary search destination.

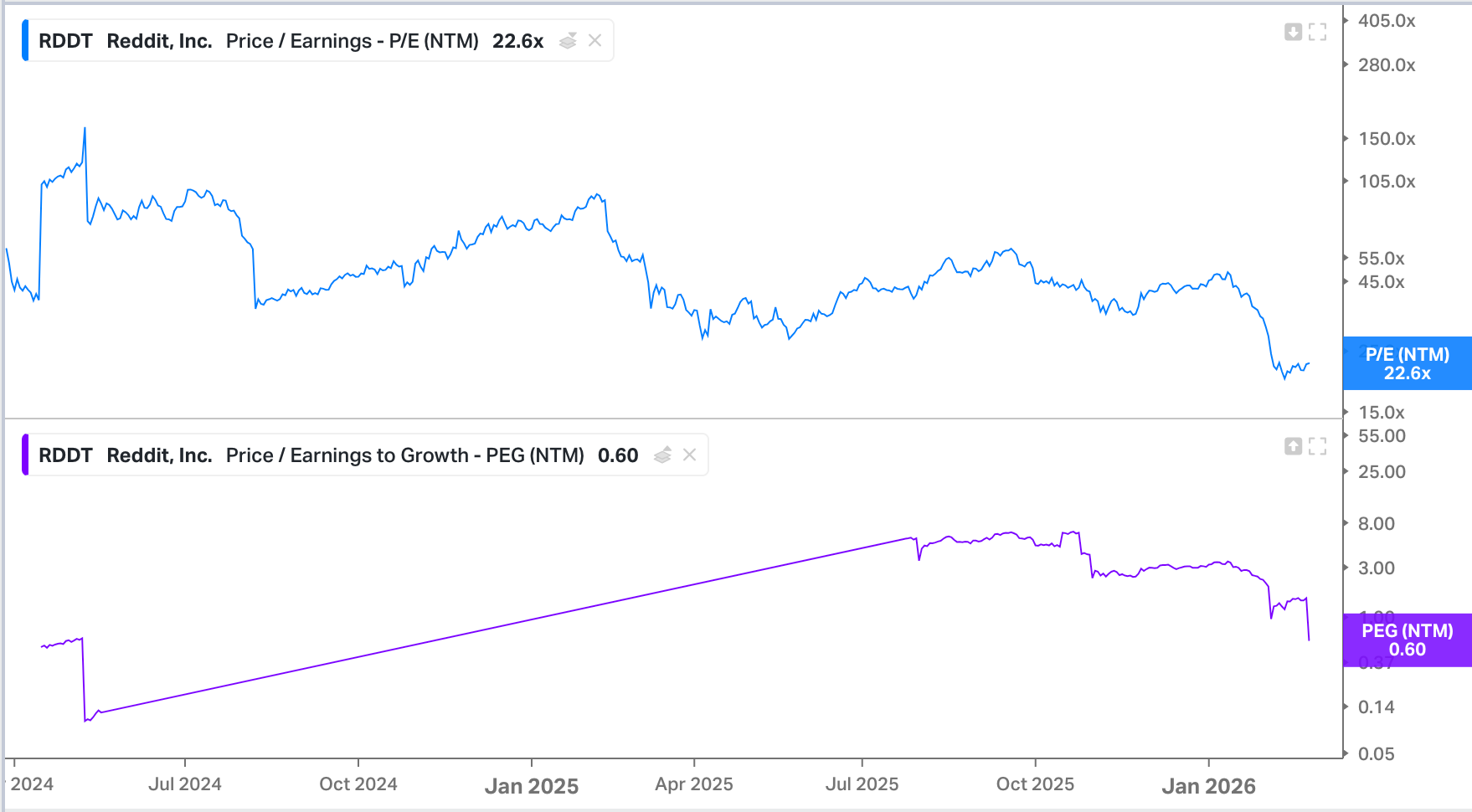

Valuation Profile

Beyond its stellar fundamentals, Reddit presents a highly attractive valuation profile relative to its growth trajectory. The stock currently trades at 22x forward earnings, despite an expected 29% top-line CAGR over the next five years. With operating margins projected to climb above 40% and DAUs estimated to double, the risk-reward setup is compelling.

Bear case

While the long-term growth outlook is strong, there are valid concerns:

The “Logged-In” Slowdown

While total DAU’s look strong, bears point to a divergence in the Logged-In US User metric.

Low Engagement Growth: In recent 2026 reports, US logged-in user growth slowed to 5%.

The ‘Lurker’ Problem: Most of Reddit’s growth is coming from logged-out users arriving via Google. These users are more difficult to monetise because they don’t have persistent profiles for ad targeting and are less likely to buy digital goods.

It is interesting that management plan to phase out reporting on logged-in and logged-out later this year. Likely as logged-out to logged-in ratio was unfavourable.

Retention: Management recognise this as an issue and are working improve retention for new and casual users

Google Search: A Double-Edged Sword

Reddit’s explosion in 2025 was largely due to Google’s algorithm prioritising forum results. This is now seen by some as a massive platform risk.

Zero-Click Searches: Google’s AI Overviews (Gemini) are becoming so adept at summarising Reddit threads that users often get the answer on the Google page and thus do not click through to Reddit.

Gatekeeper Risk: If Google decides to change its algorithm to favour other sources, or if its own AI-generated content replaces the need for forums (I do not see this happening), then Reddit’s traffic would take a noticeable it.

AI Data Competition & Saturation

The high-margin data licensing thesis is facing its first real test.

YouTube: Recent data shows YouTube has overtaken Reddit as the most cited source in AI-generated responses (16% vs 10%). If AI models start preferring video transcripts or academic data over Reddit written content, then the value of Reddit’s “firehose” will decline.

One-Time Revenue: Bears argue that data licensing is a one time deal. Once the major LLMs are trained on the 18-year archive, the incremental value of new data will come into question.

Ad Market Fatigue (Cleveland Downgrade)

In late January 2026, Cleveland Research issued a cautious report that caused the stock to sell off.

Agency Pessimism: Large US ad agencies have reportedly reduced their 2026 spending forecasts for Reddit, citing less conviction in the platform’s ability to scale ‘Direct Response’ ads (the kind that convert to sales).

ROI Decline: Partner sentiment regarding ROI dropped from 76% to 59% in a single quarter, suggesting that Reddit’s new ad tech may be hitting a ceiling.

Insider Selling & SBC Dilution

Bears cite insider sales as being a red flag.

Heavy Insider Sales: Throughout early 2026, top executives, including CEO Steve Huffman and COO Jennifer Wong, have sold millions of dollars worth of shares albeit via 10b5-1 plans. I generally do not fin insider sales concerning, particularly when they are executed under a pre-arranged plan.

However, I would prefer to see active buying as a sign of confidence. For instance, board member Sarah Farrell recently demonstrated this by purchasing approximately 50,500 shares at an average price near $148, representing a total investment of roughly $7.5 million.. See below:

SBC: While the $1B repurchase program is a positive signal, Reddit’s heavy reliance on SBC remains a concern. In FY 2025, SBC represented ~50% of total FCF, though management has successfully reduced this burden on a quarterly basis. As shown below, the 'SBC-to-FCF' ratio is trending toward a more sustainable level:

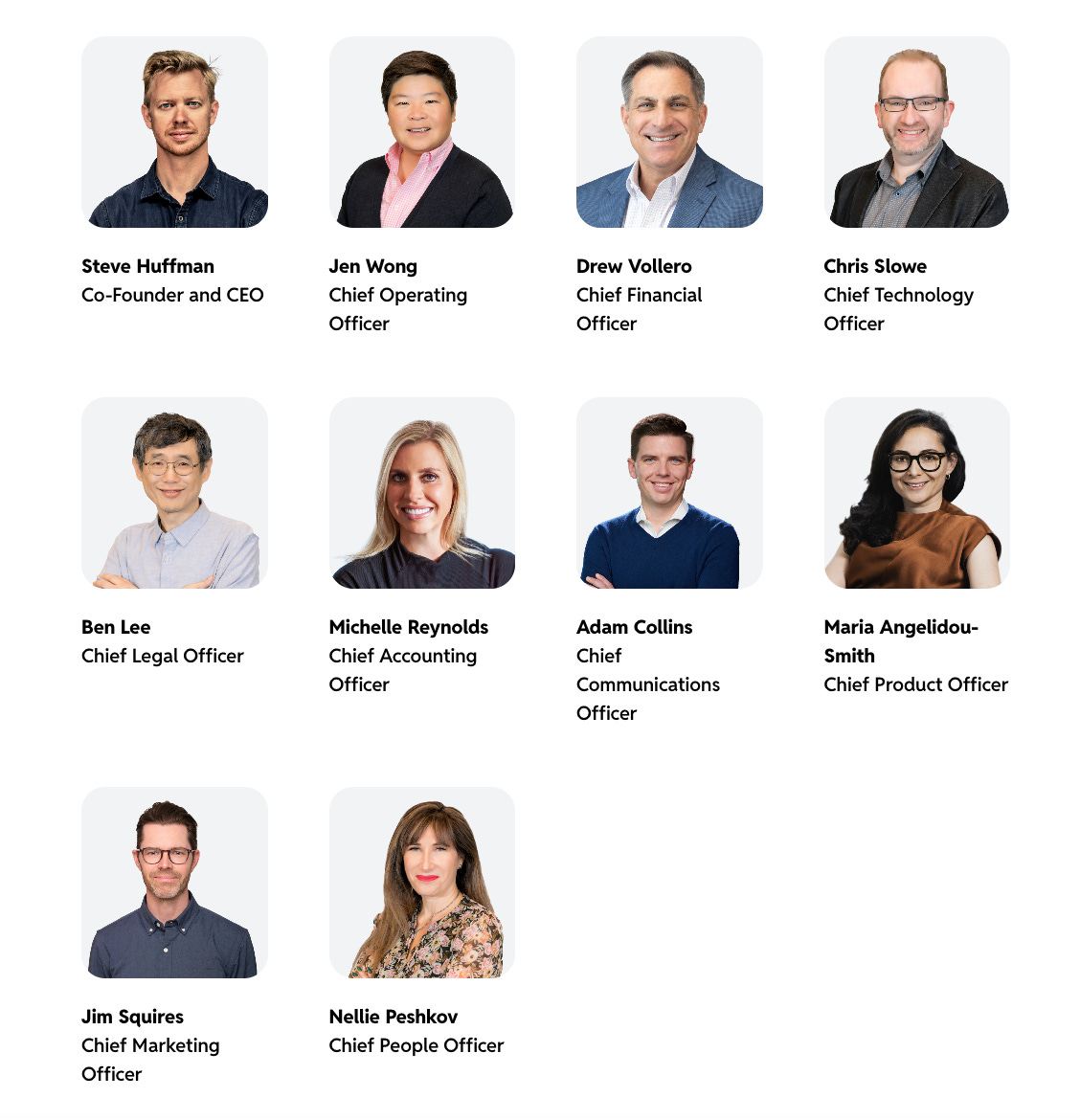

Management

Steve Huffman is the co-founder and CEO of Reddit. Huffman had a passion for programming from an early age and attained a computer science degree at the University of Virginia.

In 2005, Steve Huffman and his college roommate pitched their first startup to Y Combinator. Although their initial idea for a mobile food-ordering app called My Mobile Menu was rejected, founders Paul Graham and Jessica Livingston invited them back to build “the front page of the internet,” which led to the creation of Reddit. After selling the platform in 2006, Huffman co-founded the travel site Hipmunk and served as its CTO.

Huffman returned to Reddit as CEO in 2015. Since then, he has spearheaded the company’s international expansion, overhauled its Content Policy, and executed a full site redesign. Under his leadership, Reddit has grown to millions of daily active users engaging across hundreds of thousands of diverse communities.

The rest of the team is listed below. They are an experienced group with impressive backgrounds and resumés. Notably, CTO Chris Slowe was a Founding Engineer at Reddit and Maria Angelidou-Smith is the most recent addition to the C-suite, as the new Chief Product Officer.

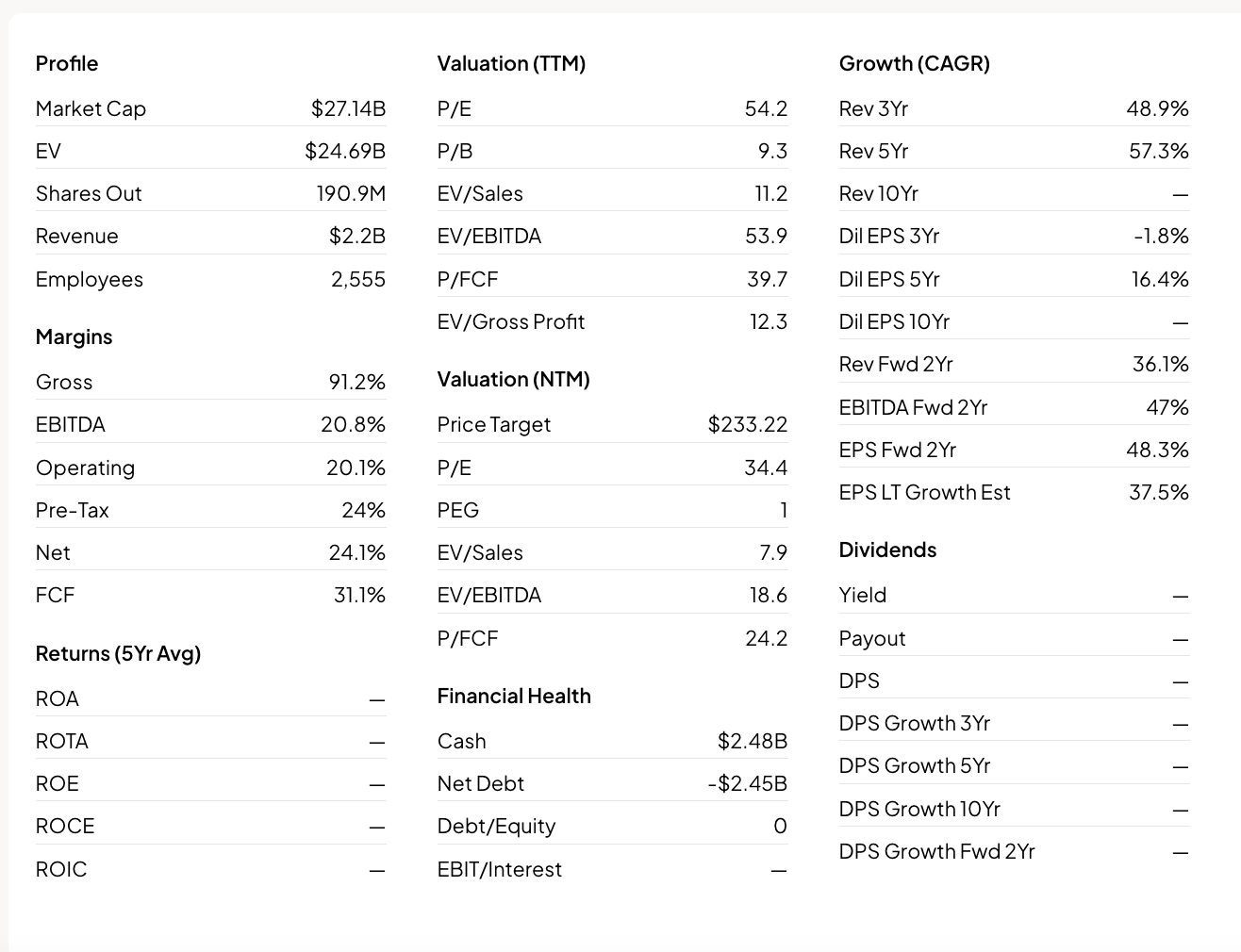

Financials and Valuation

Financials

At the time of writing, RDDT has a Market Cap of $27.14B with a Net Cash position of >$2.45B. Debt to EBITDA is -5.4.

All financials were taken from Fiscal AI’s website. You can access a free trial of the premium offering via the following link, no card required. Fiscal AI

TTM Performance:

Revenue TTM: $2.2025 (B)

Gross Profit TTM: $2.0083(B)

Operating Income TTM: $0.442 (B)

Net Income TTM: $0.5297 (B)

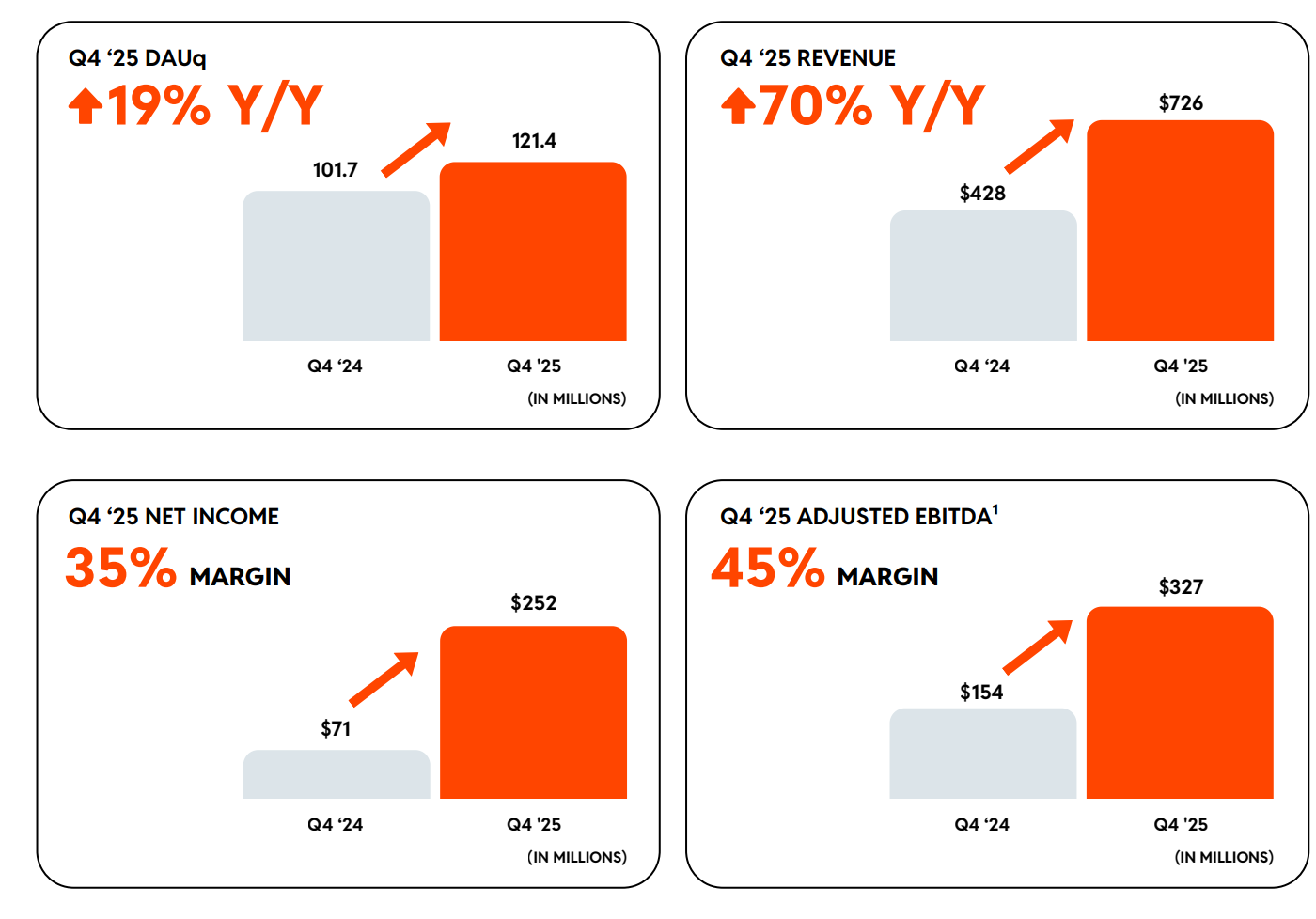

Q4 2025 Highlights: Rule of 40 score of 115%

Revenues of $726M which represented a 70% increase YOY

Operating Income of $231.8M which is up from 52.9M YOY (Q4 24)

GAAP Net Income of $251.6M up from $71M in the same period.

DAU’s grew 19% to 121M, WAU’s grew 24% to 471M.

ARPU rose 42% YOY to 5.98

Cash flow from Operations $266.8M up from $90M YOY (Q4 24)

Free Cash Flow of 263.6M (36% FCF margin) up from 89.2M YOY (Q4 24)

Management expects first-quarter revenue and adjusted EBITDA midpoints of $600 million and $215 million, respectively. We see both targets as achievable.

Valuation:

RDDT trades at:

11.2x LTM EV/S and 7.9x NTM EV/S.

53.9x LTM EV/EBITDA and 18.6x NTM EV/EBITDA

54.2x LTM PE and 34.4x NTM PE.

39.7x trailing P/FCF, 24.2x NTM P/FCF and 22x NTM EV/FCF.

Reddit is currently trading at 22x forward Non-GAAP earnings, which is particularly attractive given that the top line is expected to grow at a 29% CAGR over the next five years. Morningstar expects the company to achieve an operating margin of 46% and estimates that DAUs will double.

If one assumes the above quoted 29% revenue growth and ~40% operating margin, Reddit would reach an estimated $3 billion in operating profit. While the stock currently trades at 50x operating income, a 20x multiple would imply a market cap of $60 billion, while a 25x multiple would result in an estimated market cap of $75 billion 5 years out. Significant upside from current levels.

In our opinion, if growth and margins remain on this trajectory and achieve results near analyst estimates, shares remain significantly undervalued. If they do not, then valuations would have to be adjusted significantly.

Forward Guidance:

For the first quarter of 2026, Reddit anticipates:

Revenue in the range of $595 million to $605 million, indicating a 52% to 54% year-over-year growth, with a midpoint of approximately 53%.

Adjusted EBITDA is projected to be between $210 million and $220 million, reflecting an 82% to 91% year-over-year growth and an Adjusted EBITDA margin of 36% at the midpoint.

The total adjusted cost base for Q1 2026 is expected to be $385 million, a sequential decrease from Q4 2025.

For the full year 2026, SBC is targeted to remain in the high teens as a percentage of revenue, similar to 18% in 2025, with dilution aimed at the lower end of the 1% to 3% medium-term guide.

Chart and Technicals

Currently trades at $149.67, 25.34% below the 50SMA and 20.72% below the 200SMA.

RSI 39.42

-38.12% YTD

Reddit is currently in a downtrend with the 20 EMA trading below both the 50 and 200 SMAs, although the 50 SMA remains above a flat 200 SMA.

It is encouraging to see that selling volume has tempered recently and that the stock is holding the 126/127 level that acted as support in July. If this level is lost, then the 118 gap fill level represents a logical area to test for further support.

Since the stock is currently in a downtrend, a new entry should be made with the expectation that prices may not rise immediately without a confirmed trend reversal. One can either buy now based on long-term fundamentals while accepting the likelihood of further downside, or wait for technical confirmation. A more conservative approach would be to purchase shares only after the stock reclaims and holds the 20 EMA as a sign of a potential turn for example.

I also recommend revisiting the following post to review various strategies for buying stocks near their technical lows, it is worth your time.

Current position and plans

We currently hold a position in $RDDT with a cost basis of 131.46. Our objective is to expand this holding at favourable levels over time while utilising a trading around a core strategy to capture additional gains. To date, we have been successful in realising profits within the trading account to supplement the core position.

To receive real-time updates on our portfolio management and research, consider attaining a premium subscription below.

As a reminder a premium subscription includes:

Favourite set-up Ideas, Market Memos plus Full archive

Live Portfolio updates (All Buys and Sells) in Subscriber only Channels

Monthly in depth portfolio & performance updates

Discord access for AMAs and live trading account updates.

Thank you for reading and if you enjoyed this post, please leave a like and Restack.

Subscribe to the plan that best suits your needs (free or premium), and will see you in the next one!

Great write up, thanks.